Nayax Ltd. (Deep Dive)

Profitable market leader with a 30% growth rate, while trading at a $1.5 billion market cap

I have always admired Peter Lynch.

I don’t follow all his ideas, but I believe there are many things he preached about which are incredibly helpful for retail investors like you and me.

One of his core investing principles was that there is much more money to be made with “boring” stocks than with “hyped” businesses, as they are able to compound with less competition and trade at more reasonable valuations than the rest of the market.

“Invest in simple companies that appear dull, mundane, out of favor, and haven’t caught the fancy of Wall Street” - Peter Lynch

Today we have found a company which, while I do not find boring, operates in a niche segment of a highly profitable industry.

That company is none other than Nayax Ltd.

Nayax provides the hardware and software needed by unattended commerces to accept cash-less payments and manage operations remotely.

The company is currently active in various segments, ranging from vending machines and car washes to EV charging stations and attended retail commerces, with over 1.38 million connected devices.

This is a hard SaaS business (as it requires the installation of proprietary hardware) that is experiencing significant revenue growth and is quickly expanding its net margins.

The market is currently pricing in long-term double digit top line and bottom line growth and significant margin expansion. However, assuming that Nayax trades at the same FCF yield in the future, our DCF model points to an IRR over 20%.

Below you will find a deep dive into the business, where we cover all relevant aspects including The Compounder Score, and what i’m personally doing with Nayax.

A lot of time has been invested in researching this company for you, I hope you enjoy!

Table of Contents

Introduction

Company History

Company Overview

Industry and Market Analysis

Competitive Analysis

Bull Thesis

The Compounder Score

Risks

Financials

Valuation

Concluding Thoughts (What I am personally doing)

1. Introduction

Unattended commerce has seen explosive growth during these past years and is expected to outpace attended retail in many sectors.

This segment allows businesses to expand their footprint into high-traffic areas while maintaining a 24/7, digitally managed operation that minimizes operational costs.

The widespread adoption of contactless payments, allows customers to enjoy self-service transactions, while businesses benefit from eliminating high labor costs.

However, accepting cashless payments is complex and to do so, companies must rely on Point-of-Sale (POS) terminals.

A commerce needs help handling the highly technical process, including secure card data capture, fraud prevention, and encryption.

The POS terminal then acts as the secure gateway, which communicates the details of the transaction to a payment processor and a bank for authorization.

Here is where Nayax comes in, as it provides a solution which allows unattended commerces to accept digital payments and remotely manage their businesses.

Currently, the company is deeply embedded into the operations of over 105,000 customers and is demonstrating significant operating leverage.

This success has allowed it to process over $1.59 billion in transaction value from over 1.38 million connected devices, mainly in North America and Europe.

2. Company History

2005-2015: Founding and Rapid International Expansion

Nayax was founded in 2005 in Israel by Yair Nechmad (CEO) and David Ben Avi (CTO).

Their initial vision was to revolutionize the unattended retail market (mainly vending machines), by introducing cashless payment solutions.

However, it wasn’t until 2010 when Nayax started gaining traction, with the introduction of its Vending Supervisory Routine (VSR), which combined payment with a machine monitoring system.

This key differentiator is what incentivized Nayax to conduct an early international expansion, as the company opened offices in China in 2011, in USA in 2012, in UK in 2014, and in Germany and Japan in 2015.

In 2015, Nayax’ Monyx Wallet was launched, a proprietary consumer payment and loyalty application and that same year, the company shipped 43,000 POS terminals.

2016-2020: Accelerated Growth and Product Innovation

Early in 2016, Nayax acquired VendSys, a developer of vending management software, strengthening its position in the US market and its portfolio breadth.

In 2018, Nayax launched the VPOS Touch, a more sophisticated payment device featuring a touchscreen, multi-lingual support, and voice interaction.

Additionally, the company was issued a Payment Institution license by the Board of the Bank of Lithuania, enhancing its financial and regulatory capabilities in Europe.

In 2019, Nayax acquired Modularity Technologies Ltd., a company specializing in retail software, and launched the VPOS Fusion and Onyx devices, expanding its technological leadership.

At the end of the decade, the company reported revenues of $14.4 million and processed about half a billion transactions, with over 370,000 connected devices globally.

2021-2025: IPO and Aggressive M&A

2021 started with Nayax completing the largest-ever tech IPO on the Tel Aviv Stock Exchange (TASE), raising $210 million at a $1 billion valuation, which was expanded in 2022 as the company achieved a dual listing on the Nasdaq under the NYAX ticker.

Most these funds were directly put to work into R&D and later that same year, Nayax acquired Weezmo, marking a strategic entry into the attended retail loyalty space, and the company launched Nayax Energy for EV charging solutions.

In 2023, Nayax completed various acquisitions, with the most contrasting one being the acquisition of Retail Pro International, focused in retail POS software, entering the attended retail market.

In 2024, Nayax reported a strong fiscal year with revenue growth of 33% to $314.0 million, achieving its first profitable quarter.

At year end the company had 1.38 million connected devices and over 105,000 customers in over 120 countries.

2026 Onwards: Synergies and Vertical Expansion

Nayax’s immediate focus is on integrating the recent acquisitions to realize synergies and cross-selling opportunities, especially among its higher growth regions (e.g., Brazil).

With a strong balance sheet and its consolidated finance division, the company is positioned to monetize its vast data lake by offering financial services directly to its rapidly growing customer base.

With a 30% revenue growth guidance for FY2025, with at least 25% expected to be organic growth, Nayax’s objective is to become the market leader in its less mature markets (EV charging and Brazil).

3. Company Overview

Value Proposition

Nayax’s mission is to establish itself as the leading commerce enablement platform, which optimizes traditional unattended machines.

The main value lies in a significant return on investment achieved by enabling scalability through the reduction of operational costs and acceptance of digital payments.

The benefits of this approach can be grouped into two categories:

Increasing sales volumes by capturing transactions from consumers who prefer digital payments and enabling loyalty programs to drive repeat business.

Minimizing manual interventions and maximizing asset uptime through real-time telemetry (remote diagnostics, inventory monitoring).

How Nayax works

The integration of Nayax into a commerce’s operations, transforms the business, minimizing increased involvement from the operators.

An unattended commerce which has recently subscribed to one of Nayax’s plans, will initially receive the specified hardware, such as the VPOS Touch or the Onyx.

A technician or the owner will be able to directly install the devices using their plug and play capabilities to physically connect the device to the machine’s control board.

To ensure the correct installment, the commerce will have to log into the Nayax Core web portal and register each device’s serial number, machine names, the price for each item or service, and configure the payment flow (e.g., “tap to pay and start”).

After review by the Nayax team, the business will be able to function without any disruption, while accepting digital payment from its customers.

Every card swipe will be instantly processed by Nayax, which will deposit the sales on a weekly basis, eliminating the need for staff to physically collect cash and make bank deposits.

Additionally, the operator will be able to see the sales volume of each machine, their current status, and even remotely adjust prices, all from the website or mobile app.

This app includes inventory and machine status tracking, allowing businesses to maximize uptime through restocking and maintenance optimization.

Products and services

Nayax is a hard-SaaS company which provides proprietary hardware devices to its customers, which will enable the use of the company’s software.

These solutions are delivered through subscription plans that bundle the company’s hardware depending on the tools requested by the client.

This approach supports a “land-and-expand” strategy, making it simple for customers to verify the benefits of Nayax’s services before scaling it across their entire commerce.

We can divide Nayax’s offerings into three distinct categories:

Hardware (Physical Devices)

This segment enables Nayax’s customers to benefit from the company’s payment processing and business management capabilities.

The flagship products, such as the VPOS Touch and Onyx devices, are designed to be durable and weather-resistant to minimize the need for maintenance.

Nayax’s devices support over 80 payment methods, including all major cards, NFC wallets (Apple Pay, Google Pay), and even local QR codes (e.g., Alipay, WeChat Pay), and allow for real-time telemetry.

Beyond traditional vending, Nayax has expanded its hardware portfolio to capture higher-value segments, with the Nova Market self-checkout kiosks and Nova Smart Cooler tailored for the unattended food service verticals.

These larger terminals incorporate scanners, scales, and touchscreens, enabling a smooth self-checkout experience that handles complex pricing models not possible with a small card reader.

This diverse range of hardware products are essential to create the company’s high switching costs, which allow Nayax to generate the high-margin revenue that follows.

Software (Recurring SaaS)

This segment contains Nayax’s true differentiator and the source of its recurring, high-margin revenue through its platform, Nayax Core, and its mobile app, MoMa.

This platform acts as the operator’s real-time, remote business management system, centralizing data, such as machine health, fault diagnostics, inventory levels, and sales performance, from every connected device worldwide.

This solution fixes the “operational blind spot” inherent in unattended commerces, optimizing efficiency and performance, by for example, alerting when a best-selling item needs restocking.

Additionally, operators may change prices remotely and set up dynamic discounts directly from the Nayax Core platform, something which was unheard of before.

The platform can be tailored to the specific machines that the operator runs, whether they are EV charging stations, laundromats, micro markets, or more.

But as an investor, the best part of this revenue source is that, since it is subscription-based, it provides stability and predictability which reduces the cyclicality risk inherent in payment processors and allows for a disciplined capital management.

Financial Services (FinTech)

This segment is the company’s main revenue driver, lead by its payment processing services.

Simply put, Nayax receives a fee out of every transaction that it helps process, commonly known as the Take Rate, which is currently 2.7% of its Total Transaction Value (TTV).

Beyond basic payment processing, Nayax drives repeat business through its loyalty solutions, mainly via the Monyx Wallet consumer app.

This allows operators to create promotional campaigns and digital rewards, which may be converted into spendable currency across the operator’s entire network.

Additionally, the company is able to increase the overall LTV even further through Nayax Capital, which provides small business loans through a transparent underwriting process, as Nayax has full access to the operator’s financials.

How Nayax makes money

Nayax’s money-making strategy is built on three distinct pillars: Processing Fees (Take Rate), Subscription Revenue (SaaS), and Hardware Sales.

The most dominant source is the Take Rate, which is the percentage Nayax collects on every digital sale processed across its global device network.

This revenue stream is highly attractive as its take rate is currently 2.7%, and can be generated without requiring further CAPEX once the device has been deployed.

This take rate has seen strong growth, rising from 2.51% in 2022 to 2.7% in 2024, driven by the use of smart payment routing to achieve lower acquiring costs, and leveraging the economies of scale to negotiate better terms with payment networks.

The second, and highest-margin, pillar is SaaS Subscription Revenue, which is generated through monthly fees.

The pricing is tiered according to the number of connected devices and the functionalities required by the customer, from basic telemetry to advanced tools.

Finally, Hardware Sales, the enabler of the “land and expand” model, provides necessary upfront revenue, typically generating a 30% margin on one-time payments.

Since these sales are key to gaining access to a customer’s business, Nayax prioritizes subsidizing these initial sales through strategic pricing and offering financing solutions to guarantee long-term, recurring revenue.

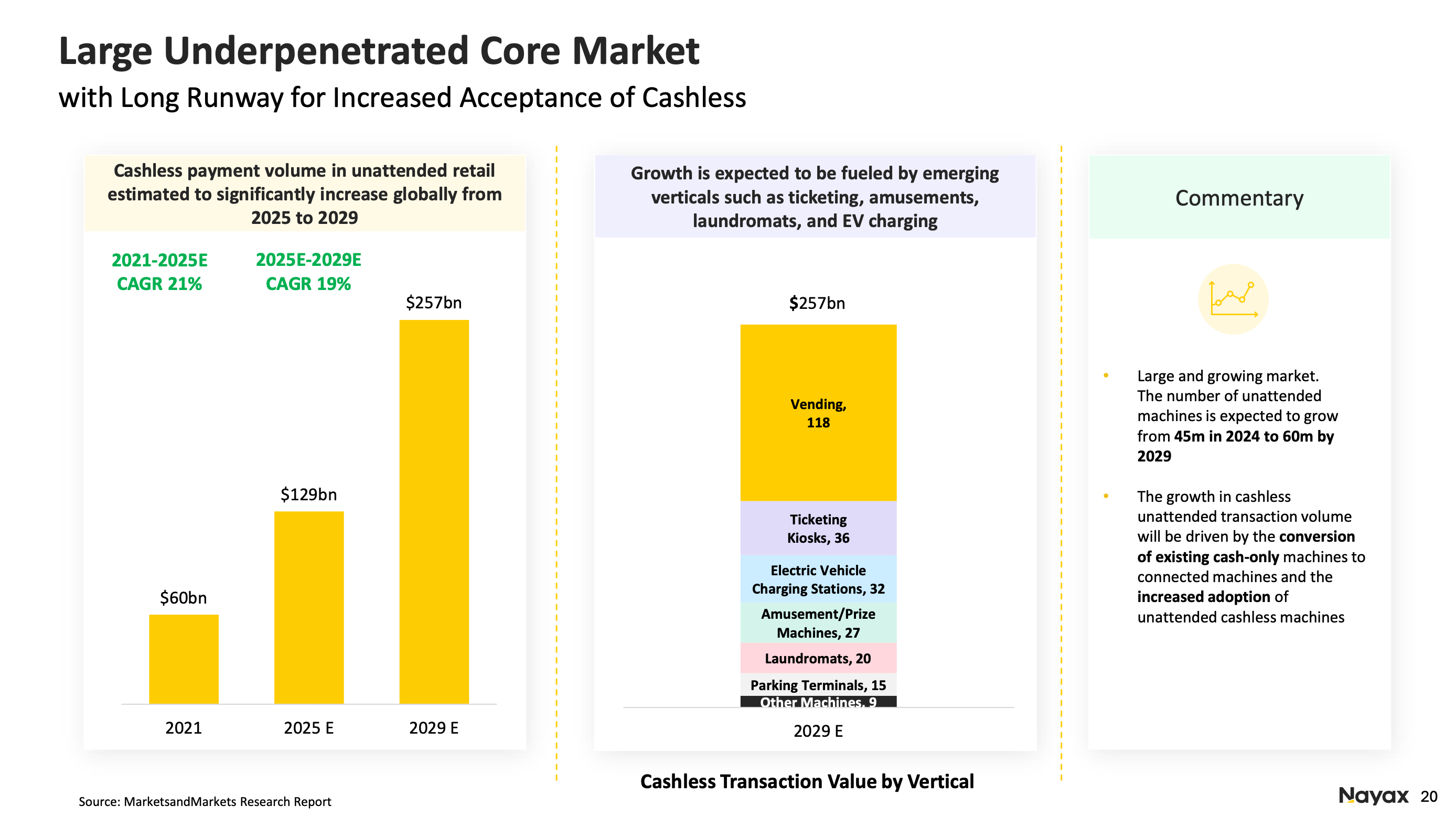

4. Industry and Market Analysis

Nayax is addressing a massive, high-growth industry that represents a TAM valued at over $129 billion, estimated to grow at a 19% four-year CAGR:

This growth is expected to be fueled by emerging segments such as ticketing, amusements, laundromats, and EV charging, all markets which Nayax has actively been positioning itself in during the recent years.

5. Competitive Analysis

Competition

The payment processing market is highly competitive and fragmented, but Nayax’s competition can be grouped into three specific categories:

Generalist Payment Processors

This category includes large, established fintech players like Square, PayPal, Adyen, and traditional banks, which offer robust payment processing services with a high brand recognition due to their massive scales.

They pose a challenge by being able to offer more flexible and competitive take rates or trying to push their own generic POS hardware.

However, their main weakness is their lack of specialization as their devices typically do not have the durability or required protocols to cater to external, unattended machines.

Additionally, since these providers generally do not offer the integrated telemetry, inventory management, or specialized loyalty tools, Nayax’s solution is more attractive to operators who want to optimize their commerces.

Specialist VMS and Telemetry Providers

This group consists of companies focused on enabling digital transactions and telemetry to the self-service industry, such as Cantaloupe.

integration for inventory management")

They challenge Nayax on the SaaS subscription front by offering deep feature sets for operational efficiency, along with POS card readers.

However, these providers are typically more regionalized and depend more heavily on third-party companies for payment processing outside of its primary market.

This limits their maximum potential margins and strategic control over the end-to-end payment chain, compared to Nayax’s integrated network of payment licenses across over 120 countries.

Vertical-Specific Platforms

These companies offer more in-depth solutions for a specific unattended vertical where Nayax is growing, such as EV charging or laundromats

Since these players offer such in-depth solutions, Nayax is forced to maintain a high level of quality to not lose customers to these niche providers.

Regardless, Nayax offers a globally certified, open platform that accepts any form of payment and adheres to international standards.

This allows them to be better positioned to work with larger, enterprise customers, which typically generate more stable, higher-margin revenues.

Moat and Competitive Advantage

Currently, Nayax has a wide moat which mainly stems from high switching costs and its intangible assets.

High switching costs are created by Nayax’s platform, which provides everything unattended commerces may need from payment processing to extensive operational information. If a company attempted to switch providers, it would have to replace their existing hardware, which would be expensive and operationally disruptive. This has made their service highly sticky, evidenced by their low revenue churn rate of 2.8%.

Nayax possesses significant intangible assets in its proprietary technology stack and certifications. This includes telemetry, routing capabilities for payments, and their established connections to over 80 merchant acquirers globally. Their status as a recognized Payment Facilitator in multiple jurisdictions and its own MasterCard issuing license (for loyalty/rewards) represent valuable regulatory and technical hurdles for new competitors.

6. Bull Thesis

Nayax has fallen over 20% from its all-time highs, which it set in July, 2025. However, it is now a fundamentally stronger business with a much clearer path to increased profitability.

The bull thesis centers on sustaining their rapidly growing profitability, through two simple initiatives:

Aggressive, high-quality revenue growth.

Significant efficiency improvement.

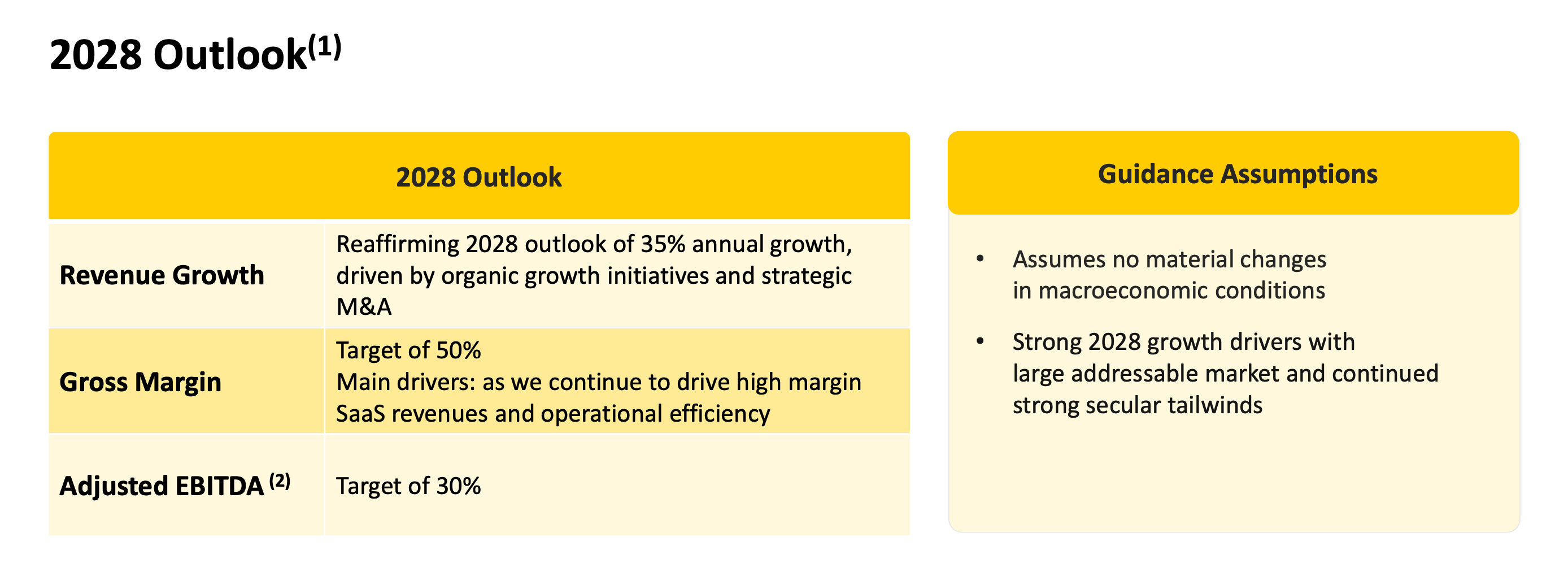

Management has established financial targets, being very ambitious with their top line and adjusted EBITDA growth:

Revenue Growth: 35% annual growth (33% YoY growth from 2023 to 2024)

Gross Margin: 50% (45% in 2024)

Adjusted EBITDA: 30% (11% in 2024)

In order to achieve their “Aggressive, high-quality revenue growth”, Nayax is leveraging different strategies which can be simplified into:

Selling more devices

Nayax’s market penetration is still relatively low, which implies that there are still significant opportunities for growth through:

Establishing partnerships with OEMs to embed Nayax’s technology directly into new machines.

Expand across high value verticals such as EV charging, and retail and hospitality.

Expand geographically to high growth markets like Mexico and Brazil.

Earning more per device (ARPU)

Nayax’s secondary driver consists on increasing their ARPU per device, which will benefit from a higher number of solutions included in their clients’ subscriptions.

Additionally, as clients scale their operations, Nayax’s ARPU will grow organically through the need for more connected hardware and a higher processed TTV.

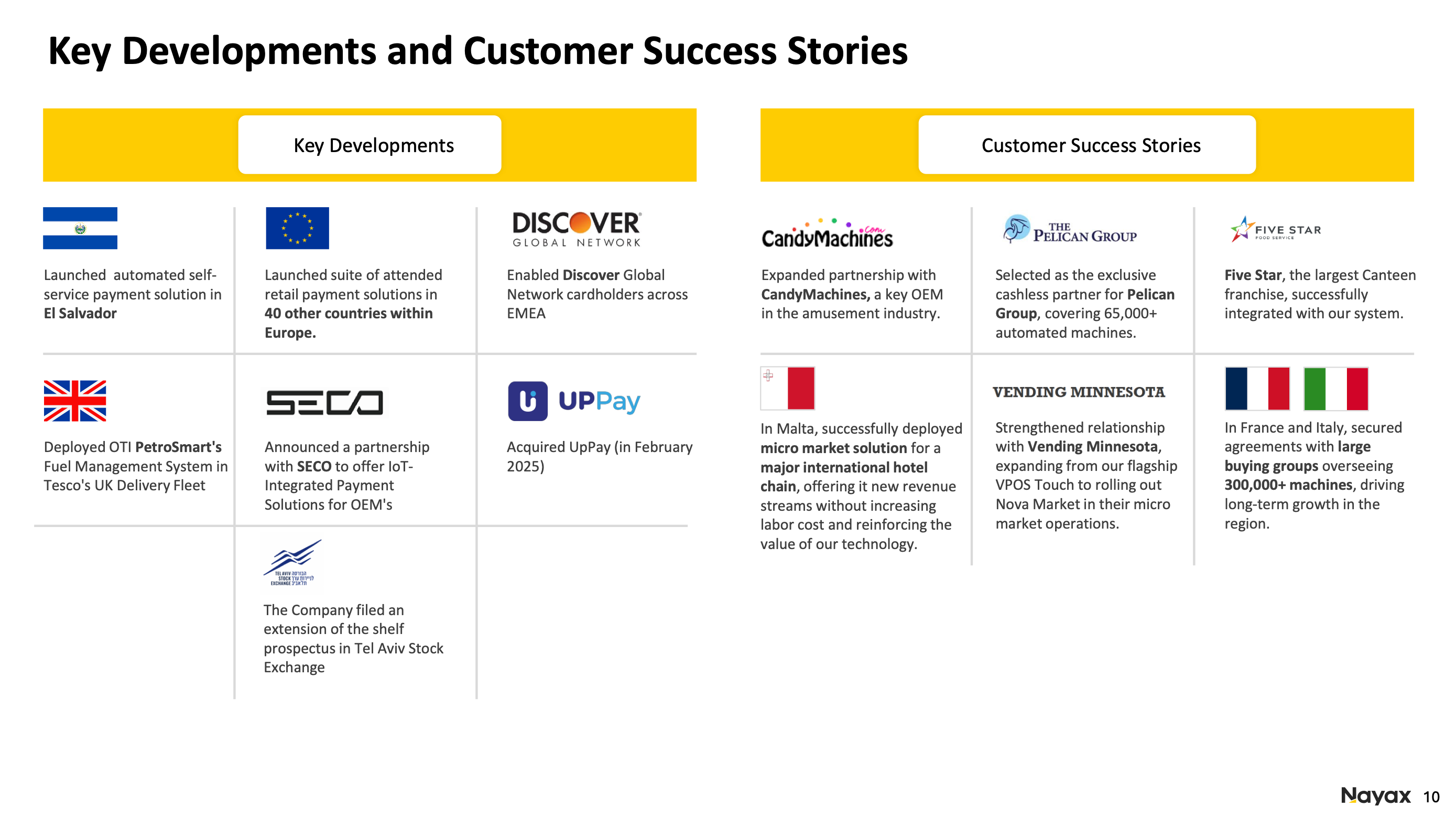

A crucial initiative to further improve this KPI is their focus on securing high-volume enterprise customers, as they have recently done with Lavazza or Autel Energy.

These larger contracts instantly drive a higher ARPU due to the demand for a greater number of connected devices, higher subscription expenditure, and substantial TTV.

Additionally, investors should track Nayax’s take rate, as it is a key lever to increase their revenue generated from their existing network of connected devices.

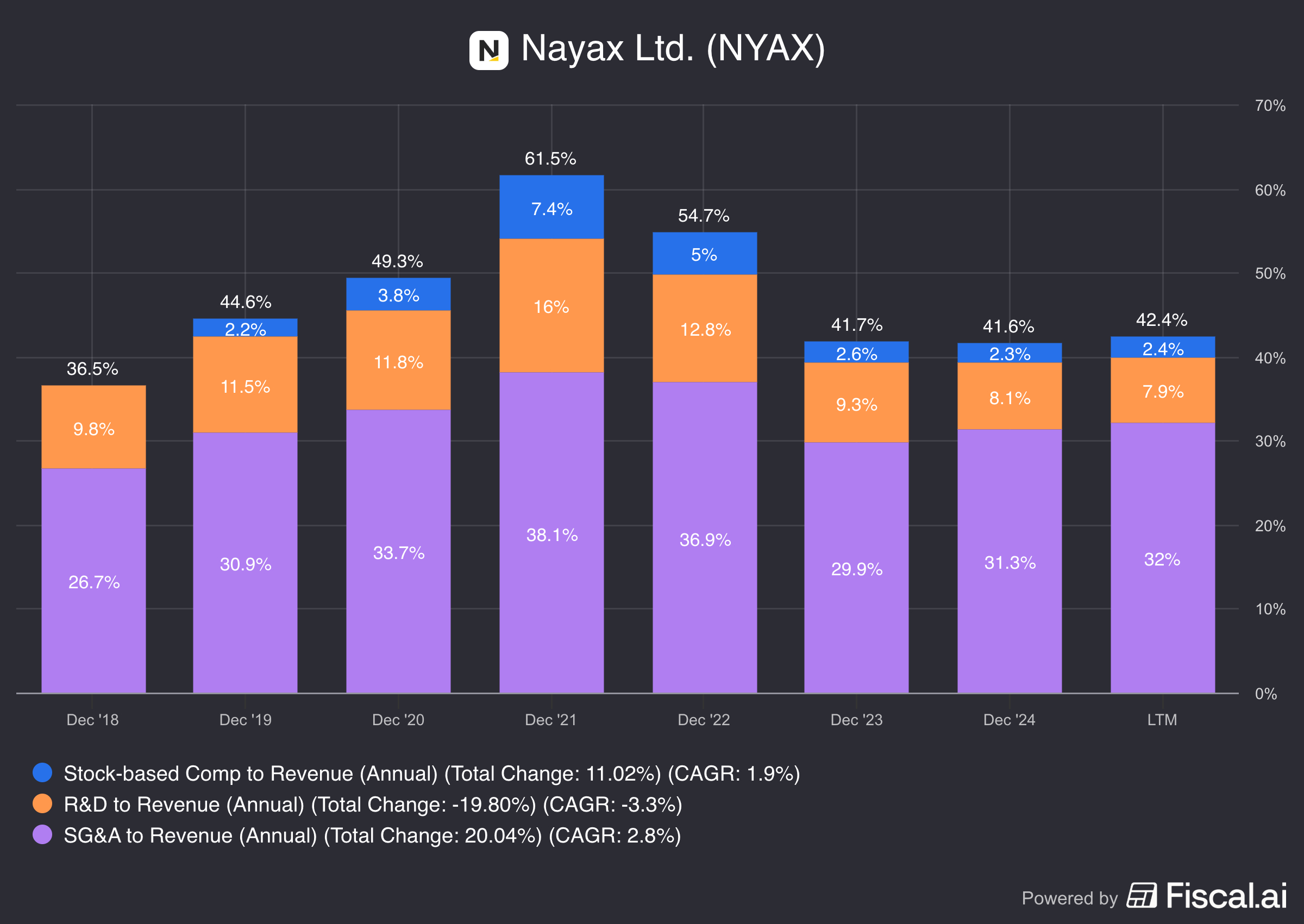

In order to achieve their “significant efficiency improvements”, Nayax must improve its OPEX as a percentage of revenues, which has fallen from 44% in 2021 to 34% in 2024.

This improvement has mainly been caused due to the company’s inherent operating leverage, which highlights that their profitability could be further improved once management implements efficiency initiatives.

I believe that Nayax has a well-laid out plan for long-term growth, allowed by their unique value proposition, and their excellent commercial execution.

In my opinion, targeting enterprise customers and focusing on securing OEM partnerships should be the company’s main focus in the mid to long term.

This would increase their revenue predictability, boost their margins, and strengthen their moat as their competitors would have a much tougher time competing for their clients.

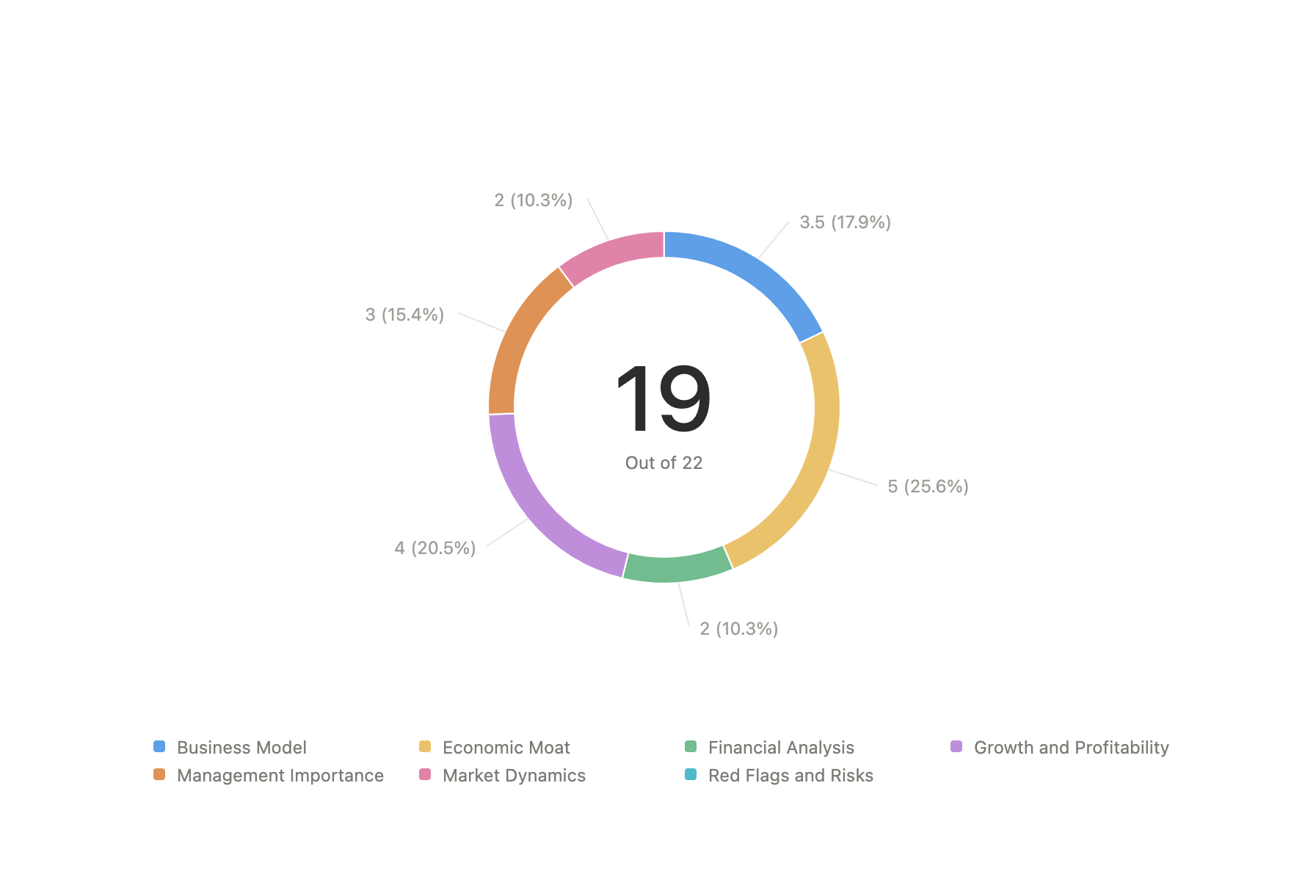

7. The CFC Quality Score

Nayax scored 19/22 on The Compounder Score, a framework for assessing companies’ fundamentals, which ranks it as a “Best-in-Class” business.

You can view the full breakdown below:

https://thecashflowcompounder.substack.com/p/nayax-the-compounder-score

8. Risks

Risk 1: Competitive Headwinds and Product Commoditization

The primary risk is the commoditization of payment acceptance hardware. As card readers become standardized and cheaper, competitors could potentially undercut Nayax on price, pressuring its margins and reducing its switching costs. If Nayax fails to rapidly scale its enterprise and OEM partnerships, it could remain dependent on smaller operators, which are more price-sensitive and have higher churn rates.

Additionally, if major global FinTech players decide to introduce VMS solutions, they could leverage their massive scale and financial resources to gain market share in the unattended commerce industry, posing a threat to Nayax’s leadership.

Risk 2: Global Regulatory and Compliance

Nayax is exposed to an extreme level of regulatory complexity and cost due to its presence in over 120 countries. Each country requires adherence to local payment regulations, where the risk of non-compliance could lead to hefty fines, suspensions, or loss of certifications, which would halt transaction revenue in affected markets.

As the company handles millions of small-ticket transactions daily, it is a potential target for cybersecurity threats and fraud. A major data breach affecting customer card data, could lead to massive financial and reputation losses. To avoid this, Nayax should continue to invest in monitoring and securing its payment infrastructure.

Risk 3: Foreign Currency Fluctuation

Nayax’s revenue is highly diversified geographically, which acts as a hedge against local economic downturns. However, this introduces significant exposure to forex volatility. Strong fluctuations between the Dollar, the Israeli Shekel, or other major currencies could lead to material losses which would impact reported earnings. However, this risk is inherent to its global growth strategy.

Additionally, since Nayax’s revenue is cyclical, it significantly depends on global consumer spending. Economic recessions, high inflation, or sharp interest rate hikes in key geographies could reduce the TTV of its existing customers, slowing the growth of its core transaction revenue. Since the company’s premium valuation is subject to its high expected growth rate, any macroeconomic headwind could lead to a rapid compression of its valuation.

9. Financials

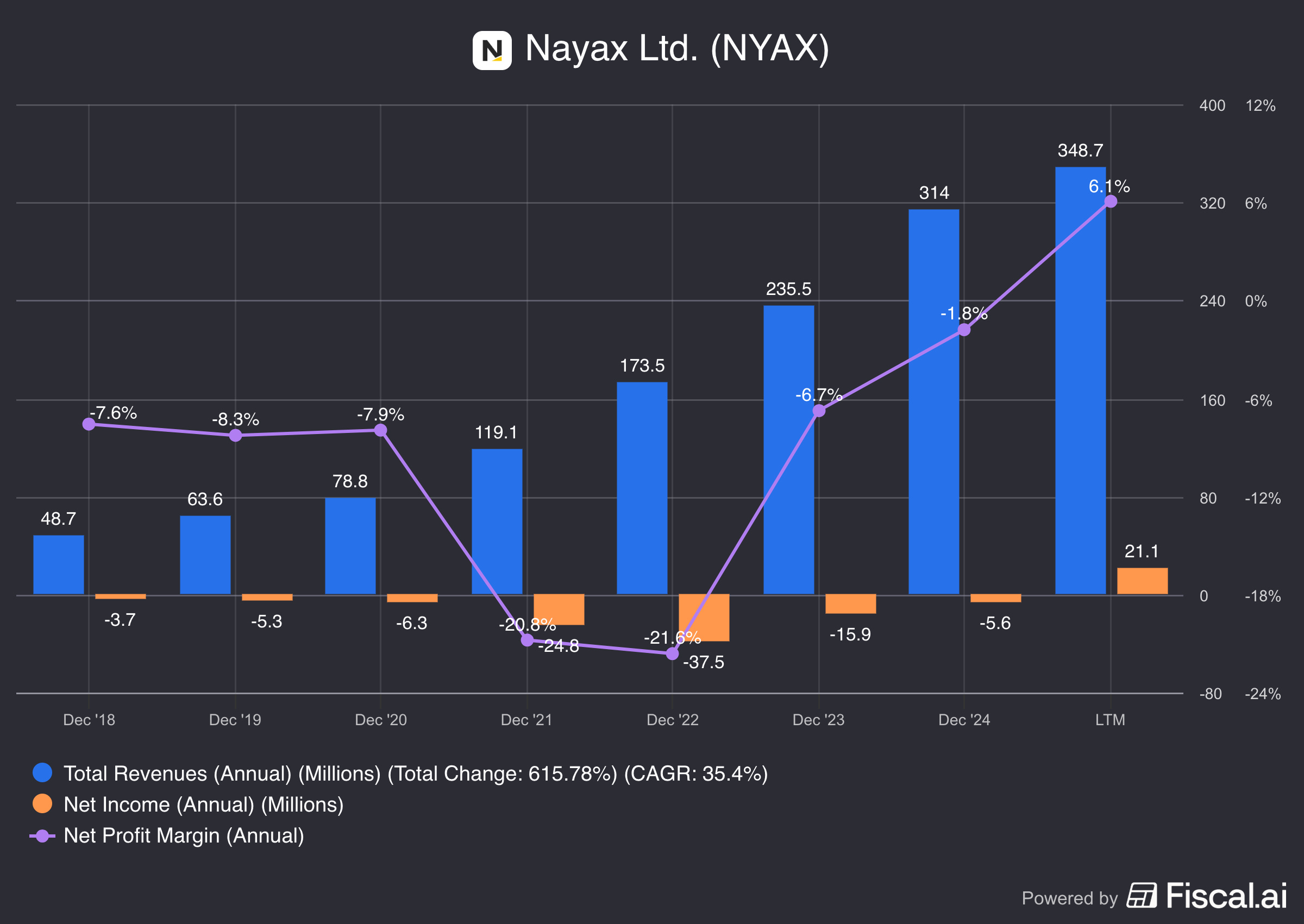

As of FY2024, Nayax reported $314 million in revenue, a substantial increase from the $236 million posted in FY2023 and representing a 38% revenue growth CAGR over the past three years.

This accelerated expansion is the result of rapid customer growth, pushing the total count past 105,000, and an expansion in the transaction volume processed, having reached $1.59 billion.

This strong top-line growth is translating into increased profitability due to the significant Operating Leverage inherent in its business model, which translates most additional revenue directly into Net Income.

As a result, Nayax has been able to expand its Net Margin from -22% in 2022 to 6.1% in the Last Twelve Months, with FY2025 expected to be its first profitable year.

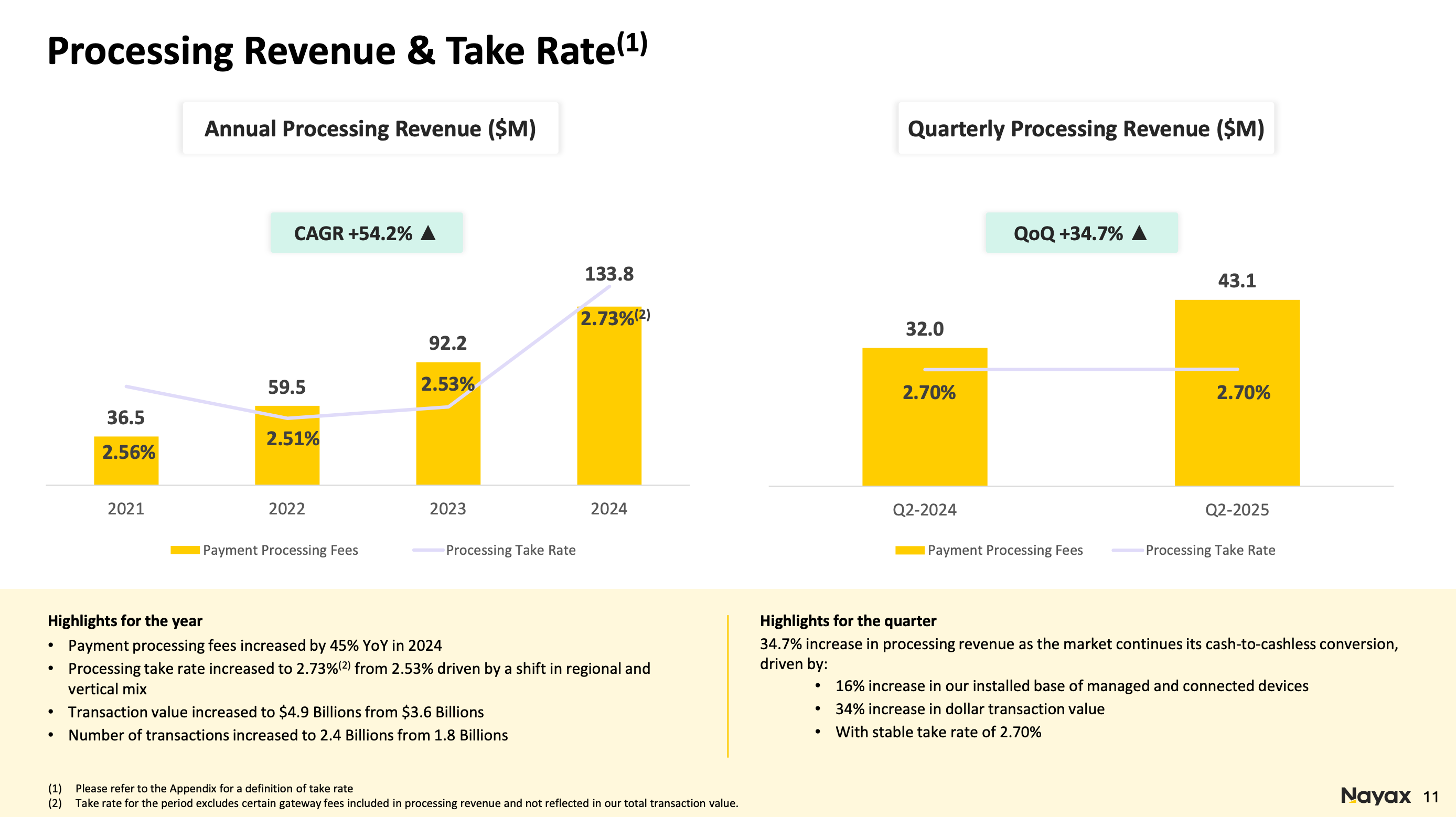

The margin expansion has largely been enabled by their strong ability to increase their annual processing revenue.

This can be seen due to their rising average take rate and the growing number of connected devices, from 1.19 million in Q2 2024 to 1.38 million in Q2 2025, a 16% growth.

Nayax is showing its commitment to long-term profitability by having reduced its OPEX as a percentage of revenue, from 62% in FY2021 to 43% in the LTM.

However, this ratio has increased since FY2023, due to the integration of its acquired companies and its high focus on expanding into new geographies and new verticals.

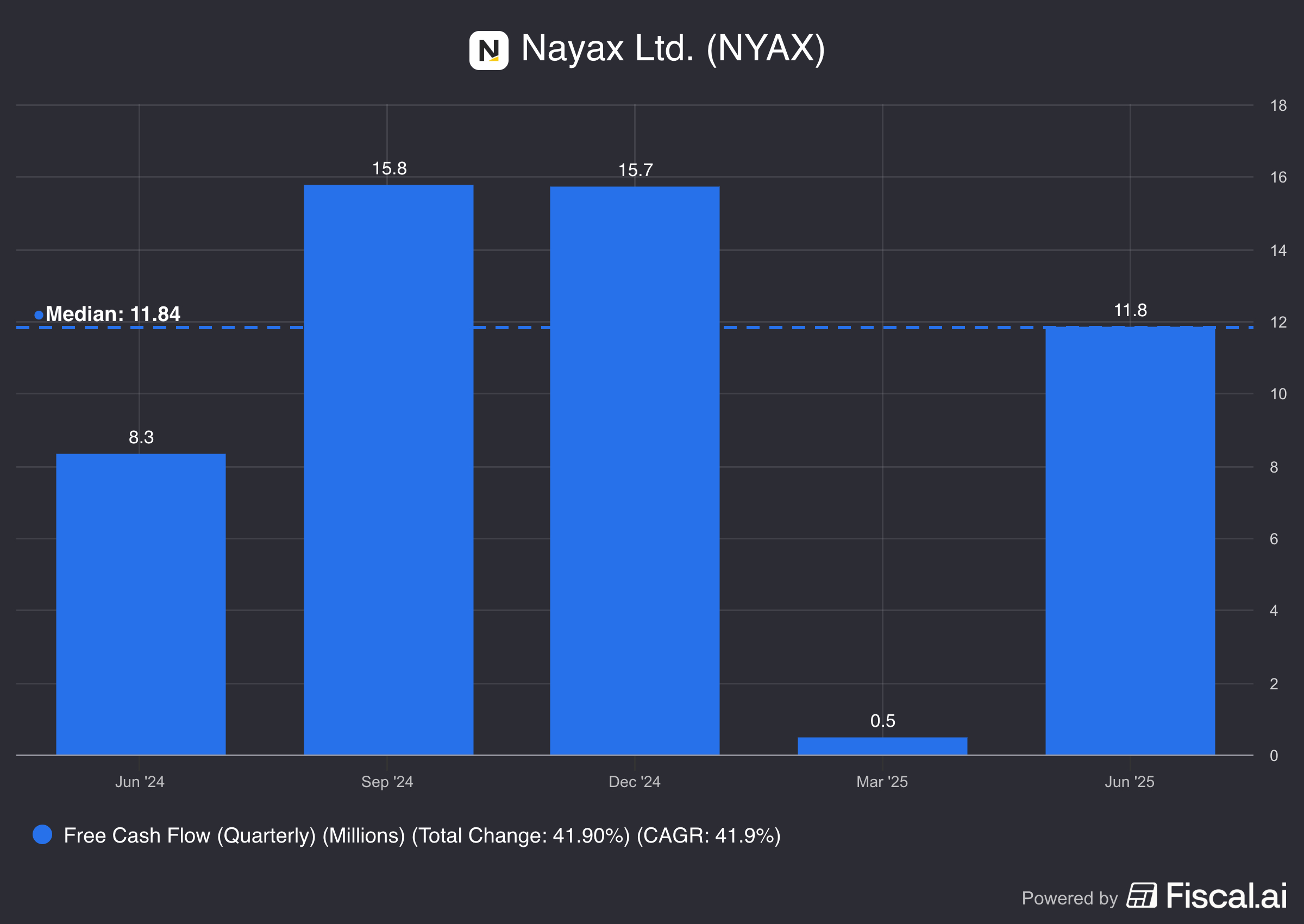

Despite recently turning profitable, Nayax has already proven its strong cash-generating ability.

The company generated over $39 million in FCF in FY2024 and has already established a record of consistent FCF generation, with quarterly results clustering around the one-year median of $11.8 million.

Finally, the company does not face the common challenge of SBC and dilution, faced by most rapidly growing software firms.

Since FY2023, Nayax’s SBC as a percentage of revenue has not been higher than 3%, proving its alignment with investors interests.

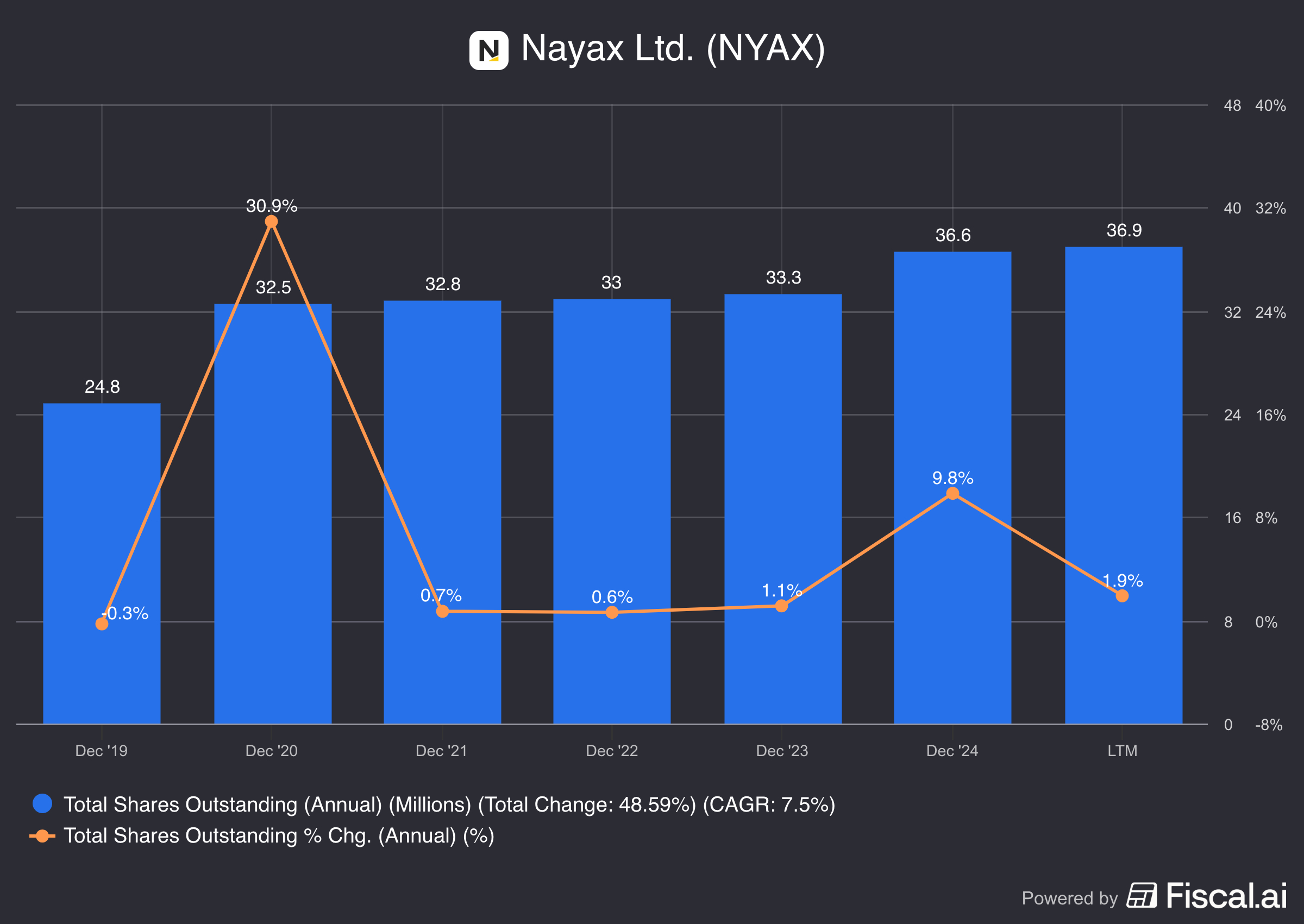

Even though Nayax diluted its shareholders by increasing its total shares outstanding by 10% from FY2023 to FY 2024, this was a one-time issuance part of the acquisitions conducted throughout the year.

From 2021 to 2023, the share count rose by less than 1.1% each year.

10. Valuation

Comparable Ratios

To analyze Nayax’s comparable and historic valuation, we can look at their forward P/E ratio, their P/S ratio, and their FCF Yield.

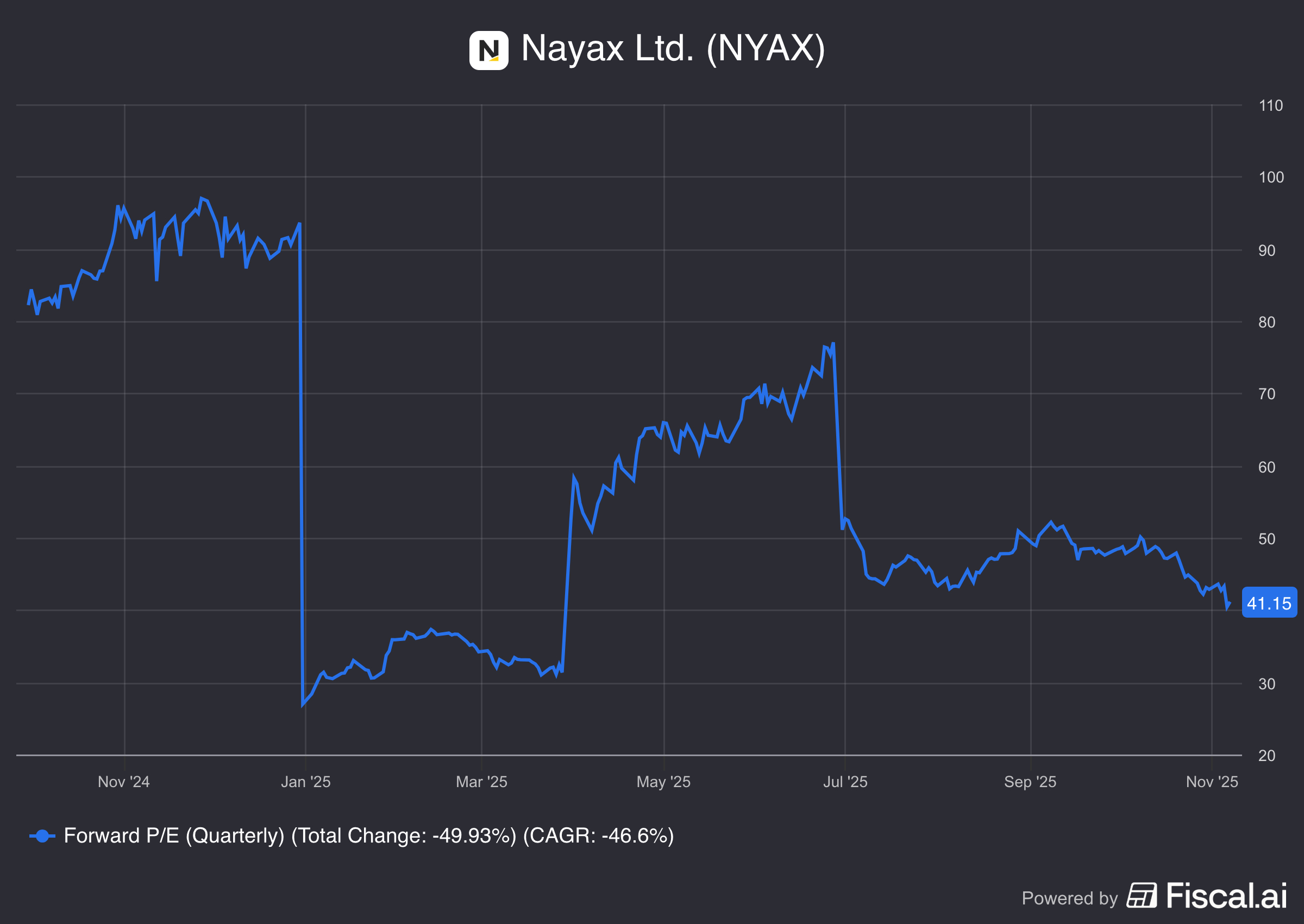

Nayax currently trades at a 41x forward P/E, which is much higher than other high-growth companies such as Toast (33.4), Adyen (36.1), or even Google (27.3).

We have to remember that Wall Street is much stricter with companies trading at high valuations. If Nayax’s top line growth were to slow down, its valuation would contract significantly to reach more conservative forward P/E levels, as it did in January 2025.

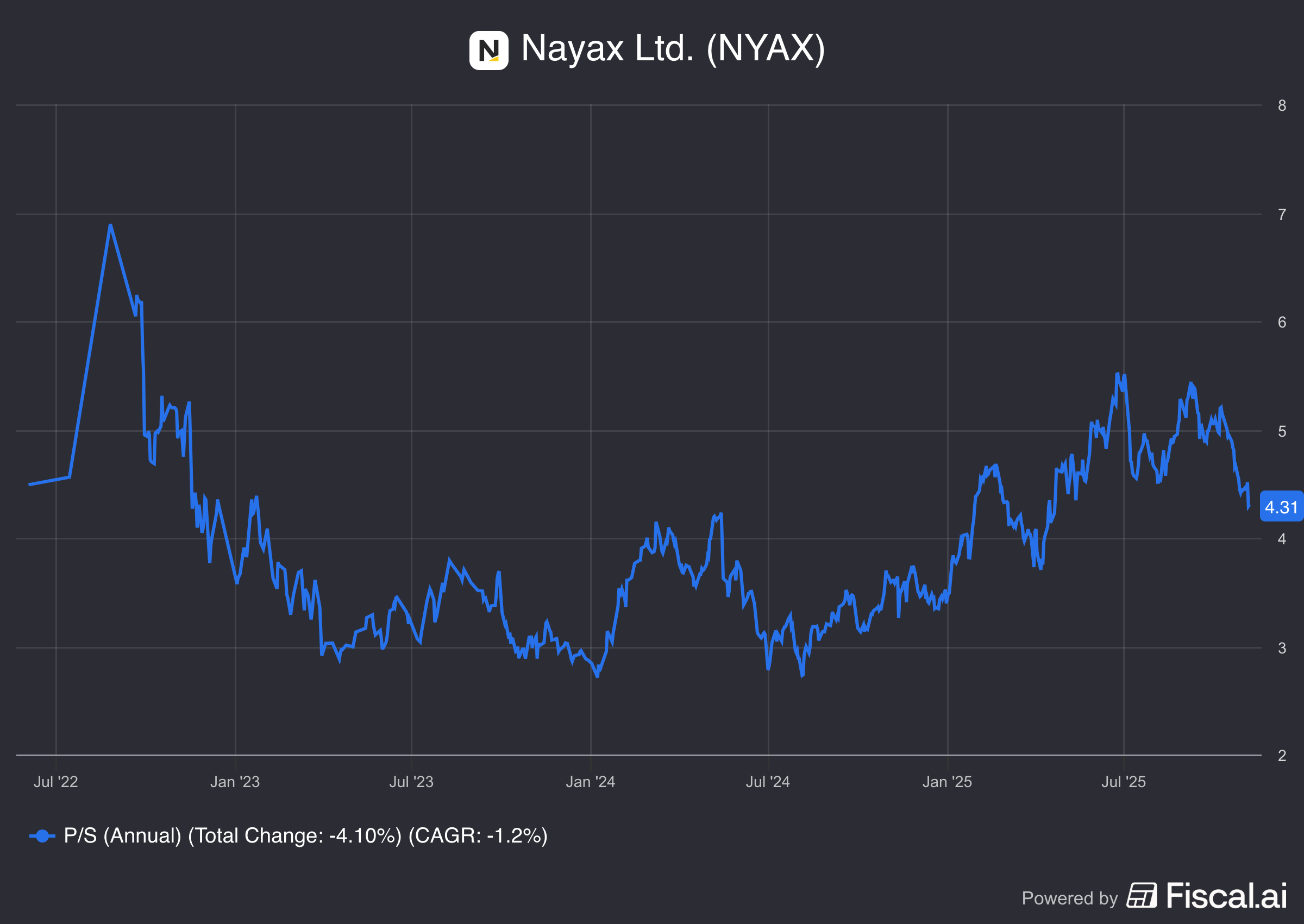

Additionally, Nayax currently trades at a 4.3x P/S, which is similar to other high-growth software companies such as Toast (4x), Lemonade (7x), and than the US Software industry’s median multiple of 3x (SeekingAlpha).

On the other hand, Nayax is currently trading at a FCF Yield of 2.9%, which is close to a reasonable long term bond yield of 3%.

As a rule of thumb, when a company trades at a FCF Yield above 3% (or a reasonable long term bond yield) and is growing its FCF generation, it could be consider as being undervalued.

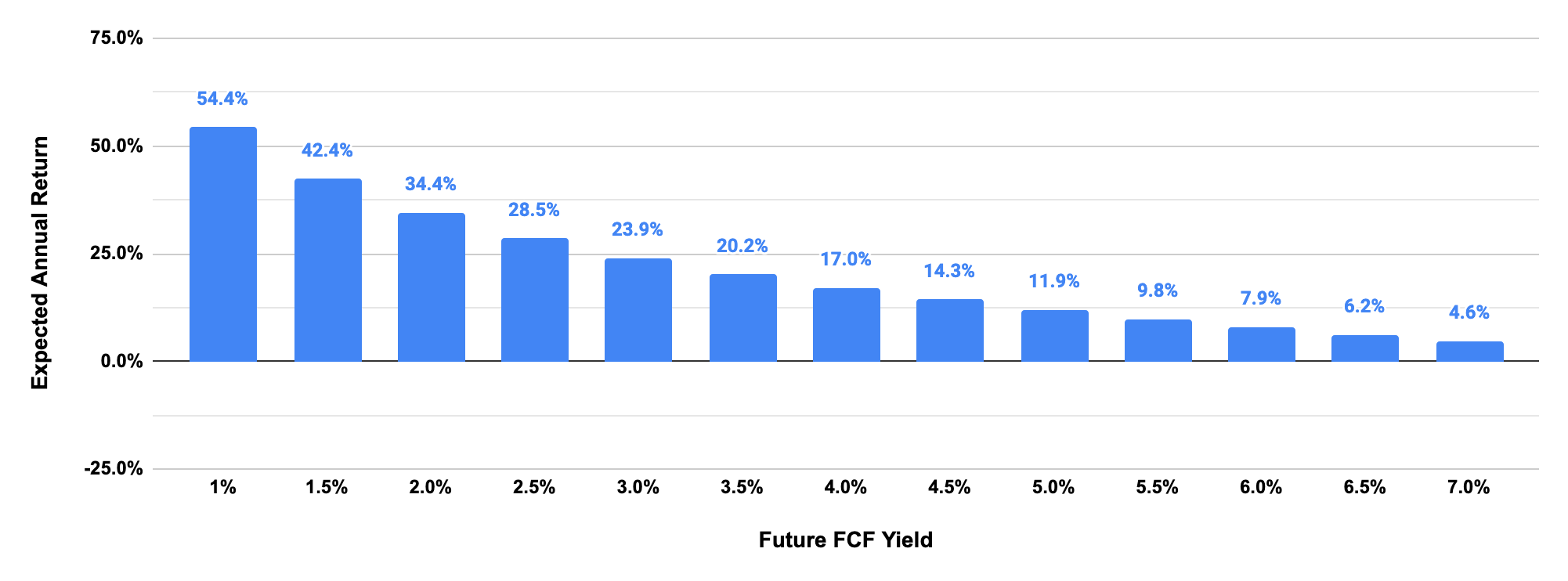

Simple FCF Model

By running a simple, highly conservative model to estimate Nayax’s future FCF, if the company traded at a similar FCF yield than its current one (3.0%), we could expect an IRR over 20%.

However, even if this company traded at a more discounted multiple in the future, at a 4% FCF yield, the expected IRR is still above 15% CAGR.

This simple model uses the following assumptions:

Revenue Growth Rate: 20% (Below analyst’s long-term estimates of 23.5%)

Operating Cash Flow Margin: 25% (Considering a conservative margin expansion)

CAPEX as a % of Revenue: 10% including fixed cost CAPEX (Higher than its latest 8% to account for increased investments in expansion efforts)

Buyback Yield: -1.5% (Slightly higher than the existing dilution to account for potential acquisitions)

11. Concluding Thoughts

Conclusion and Thesis

The Compounder Score and the Deep Dive analysis highlight a company which is leading the transition to digital payments with a highly profitable value proposition in a largely untapped industry.

It is understandable that its stock is trading at a premium due to its promising growth, high stability, and margin expansion opportunities.

The core thesis is that the company will continue to grow its customer base, expand its ARPU per connected device, and largely improve their margins through their proven operating leverage.

When considering their incredibly strong balance sheet, their estimated growth, and management’s approach towards long-term profitability, I believe Nayax represents an attractive risk-reward profile for a very patient, long-term investor.

Having said that, at the current valuation it seems like most of the positive scenario has already been priced in, without considering many of the competitive, or multiple contraction risks.

What To Look For in Earnings

The primary focus for reviewing Nayax’s future earnings releases should be any developments in the following:

Number of connected devices as it is the leading indicator of future recurring revenue.

Customer growth rate to validate market share capture and effective commercial execution outside of existing relationships.

ARPU per device and Take Rate to understand Nayax’s ability to up-sell the high-margin SaaS features and improve their routing efficiency.

Dollar-Based Net Retention Rate to ensure increasing revenue from existing customers and low churn rates (typically aim for above 120%).

Enterprise and OEM updates to track the catalysts for future predictable revenue and cost-efficient growth (updates on contract wins or OEM partnerships).

Potential Deal Breakers

Additionally, I am also laying out some criteria under which I would consider exiting the position before the investment thesis plays out:

Weakness in the overall economy due to the effect it would have on investor confidence.

Sustained slowdown in connected device growth or a significant decline in the ARPU / number of customers.

Considerably lower revenue growth than estimated, specifically below the 20% range.

Unclear success in expansion into new geographies or adjacent verticals.

Failure to execute on strategic growth catalysts such as enterprise growth and new OEM partnerships.

Reversal of the strategic focus on long-term profitability, or any significant unjustified increases in operational expenses or CAPEX.

Equity offerings or other ways of significant equity dilution (Higher SBC).

What I’m Doing

Nayax is one of the only companies which have classified as a “Best-in-Class” in The Compounder Score.

It links exactly everything I look for in a business, high margin products, customers locked in through proprietary hardware, and a largely untapped, “boring industry” which currently does not have intense competition.

My primary concern is the current market valuation, which suggests a very aggressive pricing of future fundamentals. Due to this premium, the company is highly sensitive to external factors.

Any potential macroeconomic headwinds, including increases in credit default rates, unemployment, or interest rates, would significantly impact its stock price relative to the general market (induced by its premium valuation and high cyclicality).

Having said that, during the next few weeks I will be selling some of my lower conviction stocks to free up cash and start a small position in Nayax.

My objective is to closely track any developments and add to the position when its forward P/E and P/S ratios come closer to early 2025 levels.

I believe that, despite trading at a hefty valuation, Nayax looks like an incredible long-term play, which will pay-off by dollar-cost averaging into the position.

This deep dive certainly helped me better understand the investment opportunity and I hope that you were able to find it helpful,

In case you did, please consider joining our FREE subscription to not miss out on future posts!

Thank you for reading,

Best,

The Cash Flow Compounder