TransMedics Group (The Compounder Score)

High growth, profitable company with a patent portfolio extending into the 2030s

I applied The Compounder Score—a weighted framework for assessing companies’ fundamentals—as a preliminary screening tool to determine if TransMedics Group ($TMDX) warrants a full deep-dive analysis.

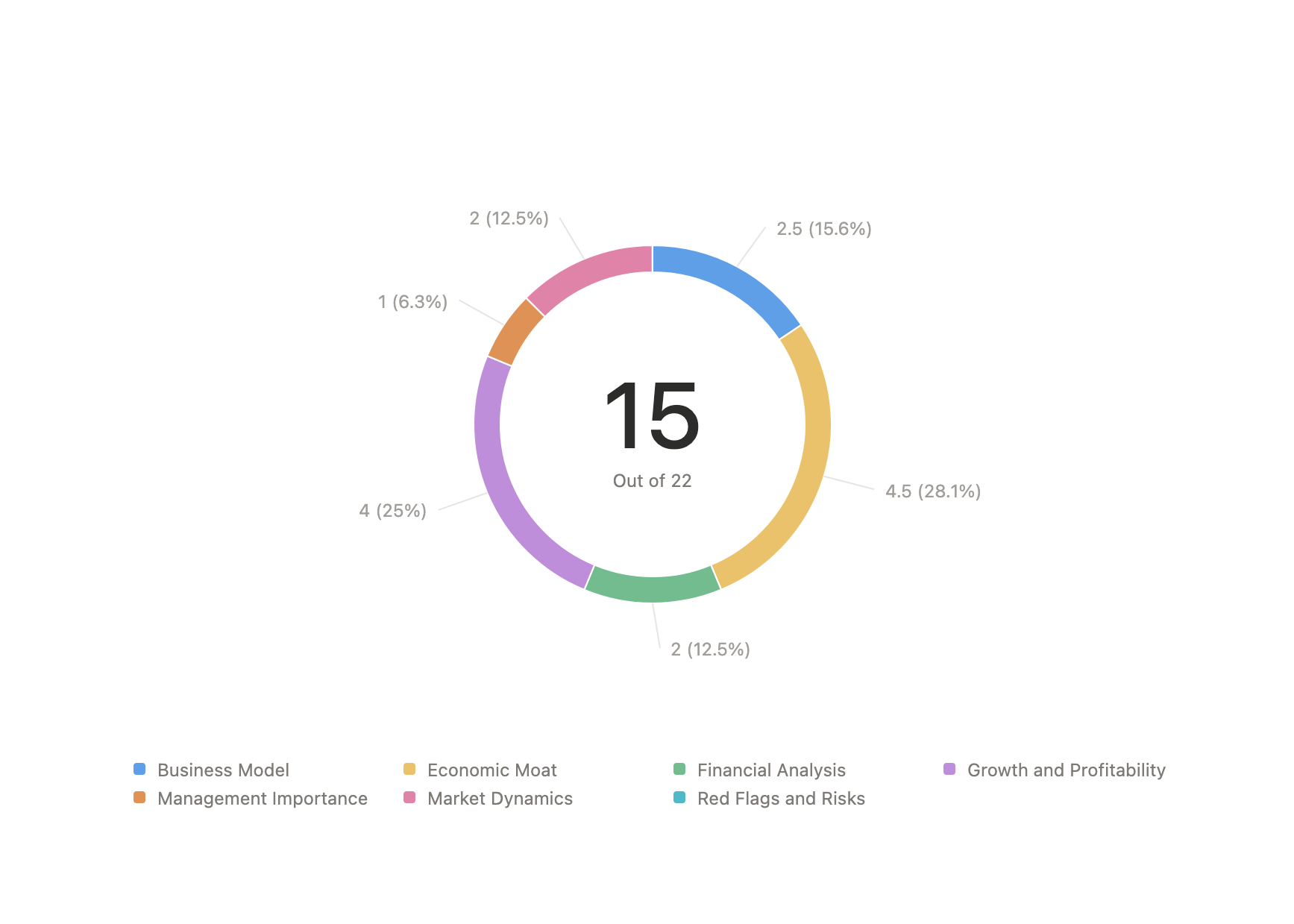

The maximum score is 22 and the ranking system is as follows:

12 and below: High Risk/Pass

13 to 15: Viable

16 to 18: High Conviction

19 and above: Best-in-Class

The Compounder Score

TransMedics Group is a medical technology company that is transforming organ transplantation with its patented Organ Care System (OCS). The OCS platform, uses warm, oxygenated, nutrient-enriched blood to extend the time an organ can be transported and allows clinicians to assess the organ’s function before transplant. This solution addresses the vast imbalance between the demand and supply for organs, aiming to expand the usable donor pool.

Leveraging its success, the company has created a comprehensive solution called the National OCS Program (NOP). The NOP provides a service that includes OCS technology, specialized staff, and logistics (including a company-owned fleet of 21 jets) to retrieve, manage, and transport organs across the U.S.. TMDX generates revenue through a usage-based model offering its services to transplant centers for heart, lung, and liver transplants. For every procedure, the company generates OCS device sales and service revenue generated from the use of the NOP, which covers the use of the device, consumables, the team, and all necessary logistics.

Let’s analyze the company by using The Compounder Score:

1. Management Importance

“Skin in the Game” and Incentives: (1/2)

According to the company’s 2025 Proxy Statement, individual insiders account for over 6.4% of the total ownership in the company, with most of this ownership belonging to TransMedics’ Founder and CEO.

RSUs and Stock Options (share-based compensation) made up 82% of the TMDX’s CEO total target 2024 compensation and 74% of the company’s average NEO, highlighting the effort made to align its management’ interests to its shareholders.

Business Resilience to Management: (0/1)

Since TMDX was founded in 1998, it has only had 1 CEO, Dr. Waleed Hassanein, which is the official founder.

The company’s business model is not simple, as its success relies on the complex combination of a patented medical device and a full-service logistics operation involving a dedicated fleet of aircraft and a nationwide network of specialized clinical staff and surgeons.

While their market position is robust due to high barriers to entry, TMDX faces a significant transition risk under a new leader, where its growth and execution would face significant disruption risks without Dr. Hassanein’s deep operational expertise.

2. Market Dynamics

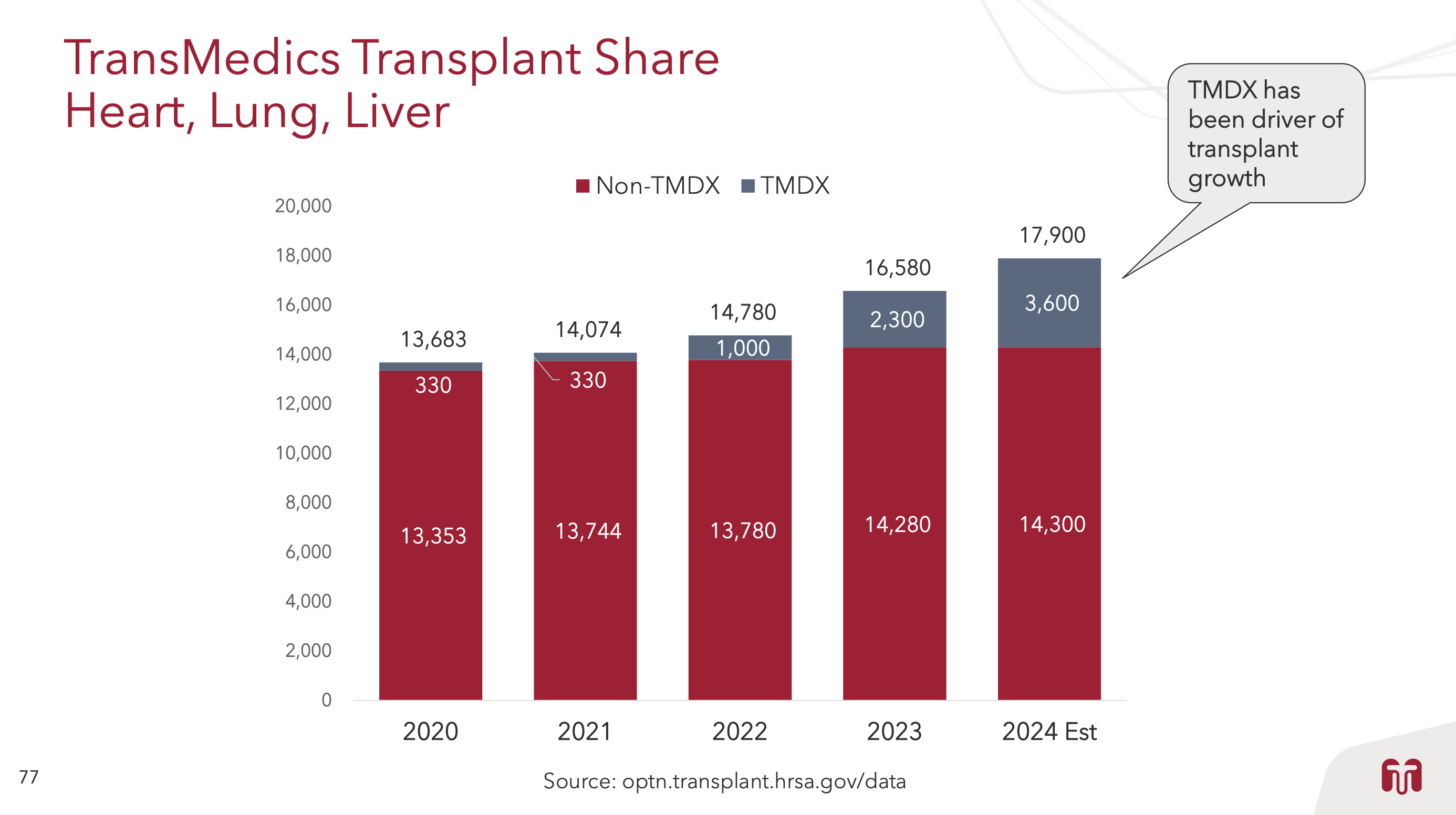

Large and Growing TAM: (1/1)

TMDX currently estimates its TAM to be made up of 17,900 yearly domestic heart, lung, and liver transplants, with an estimated four-year CAGR of 7%.

The industry’s growth is expected to be largely driven by the company’s products and services as they allow for many organs to be used in transplants, which would have previously not been used.

Exposure to Secular Trends: (1/1)

TransMedics’s offerings benefit from several powerful secular trends:

Organ Shortage: Persistent imbalance between the demand and the limited supply of suitable organs.

Normothermic Perfusion: Clinics are moving from cold storage toward warm, normothermic perfusion (TMDX’ OCS method) as it enables much longer transport times.

Aging Population: Increased prevalence of end-stage organ diseases, directly increasing the number of transplants required.

Adoption of DCD Organs: Increasing use of organs from Donors after Circulatory Death (DCD) due to technology allowing to resuscitate these organs.

3. Business Model

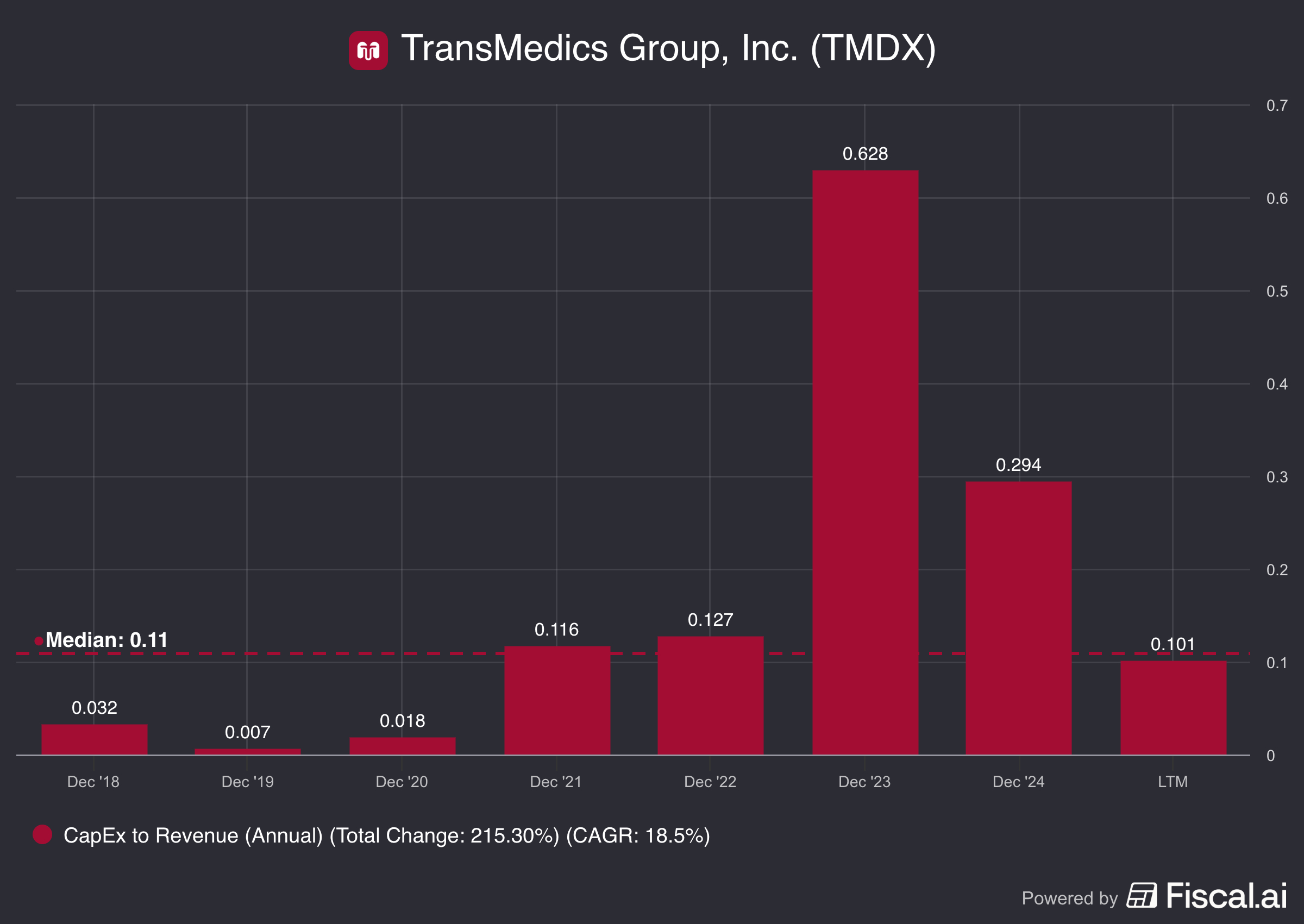

Asset-Light Model: (0/1)

TransMedics has consistently maintained a CAPEX ratio over 10% of its revenue for the past 4 years, with a median of 11%, which is enough for us to not consider them an asset-light business.

High Portion of Recurring Revenue: (0.5/1)

Even though TransMedics does not operate a subscription service, its business is highly reliant on repeat usage. The company’s customers, transplant centers have become heavy repeat users of both OCS disposable kit required for every transplant and the NOP service, which handles 91% of total U.S. OCS cases.

This demonstrates the scale of their repeated logistics and clinical support, as this business model locks in customers due to the superior outcomes and logistical ease provided.

Margin Stability / Growth: (2/2)

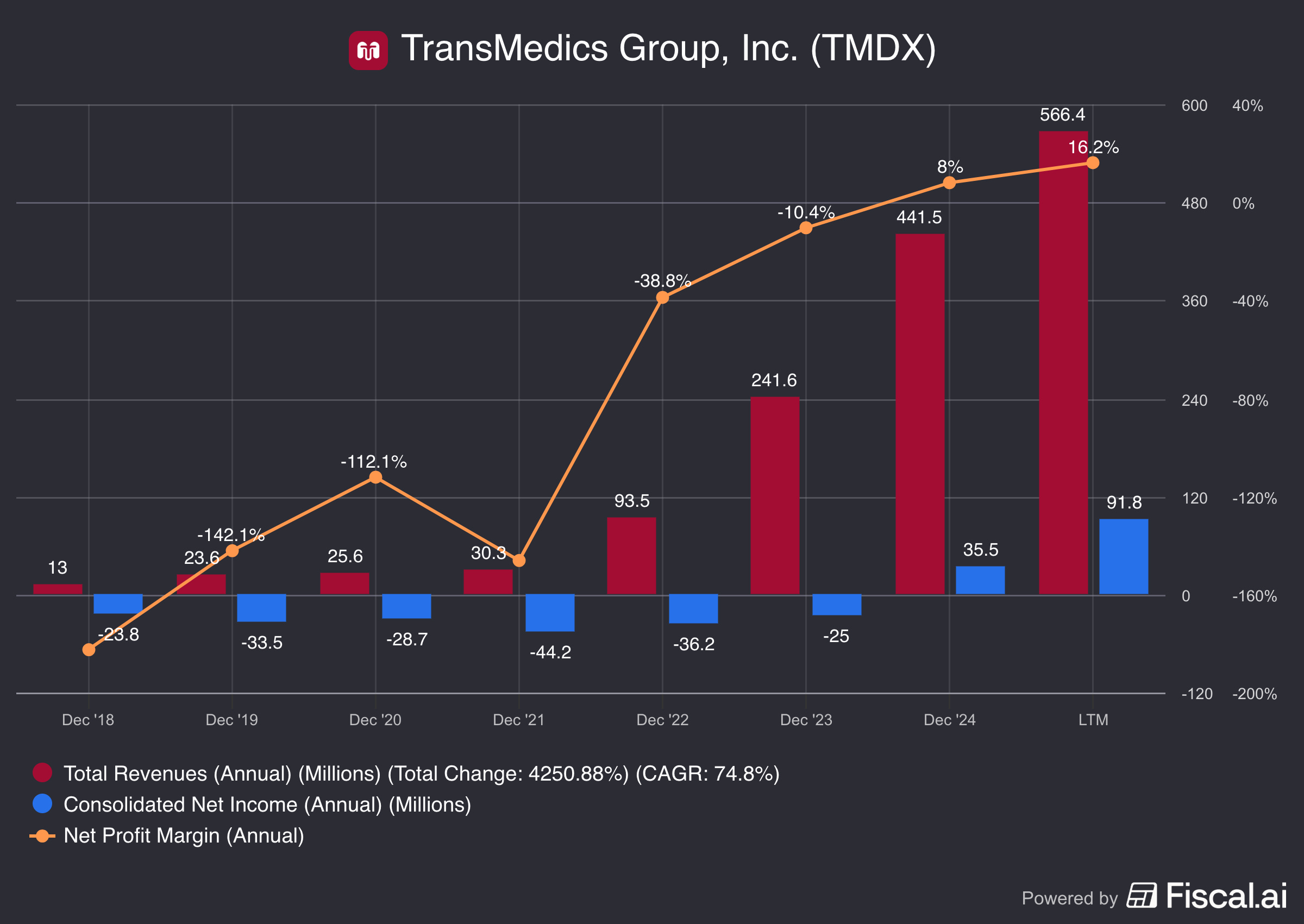

TMDX’s margins have been expanding every year since 2021, with the net margin rising from -150% to 8% in 2024 and 16.2% in the Last-Twelve Months.

4. Economic Moat

Sustainable Competitive Advantage: (2/2)

$TMDX is developing a wide moat mainly based on intangible assets and high switching costs.

TransMedics’ Organ Care System (OCS) technology is protected by a substantial patent portfolio extending into the 2030s, which essentially allows the company to be the sole producer of OCS devices. Additionally, the typical FDA approval process for such type of medical devices is lengthy, costly, and highly complex, creating a regulatory hurdle that competitors must clear to challenge TMDX’s established offerings.

On the other hand, high switching costs are created by TransMedics’ NOP, which takes care of the entire logistics process. Once a transplant center outsources its organ retrieval process to TransMedics, switching to an alternative logistics solution would be highly disruptive and riskier for clinical outcomes. Additionally, the adoption of the OCS technology requires substantial training and integration for clinical staff.

Pricing Power: (0.5/1)

TransMedics has the ability to raise its prices without experiencing a significant loss of customers, as it provides a critical, life-saving service with high switching costs.

However, the company operates in the healthcare system which is highly regulated. While TMDX can charge a premium for its technology and integrated logistics, significant price increases are limited by the necessity of reimbursement approval and the existing regulatory environment.

Dominant or Disruptive Position: (1/1)

TMDX is a clear leader within its market of normothermic perfusion, evidenced by its presence enabling over 3,600 yearly heart, liver, and lung transplants, representing a 20% domestic market share.

Additionally, TransMedics acts as a powerful disruptor as it has transformed traditional transplants by providing a solution which enables for organs to be transported for longer and for organ assessments to be conducted before the transplant.

Embedded in Customer Behavior: (1/1)

TransMedics is considered a “need-to-have” provider as it is essential for the execution of life-saving transplants, meaning that high-volume transplant centers would have to face significant logistical and clinical burdens, with a lower availability of organs. This success is evidence by TMDX’s services being responsible for 91% of total U.S. OCS cases, transplant centers become heavily reliant on the company.

5. Financial Analysis

ROCE: (1/2)

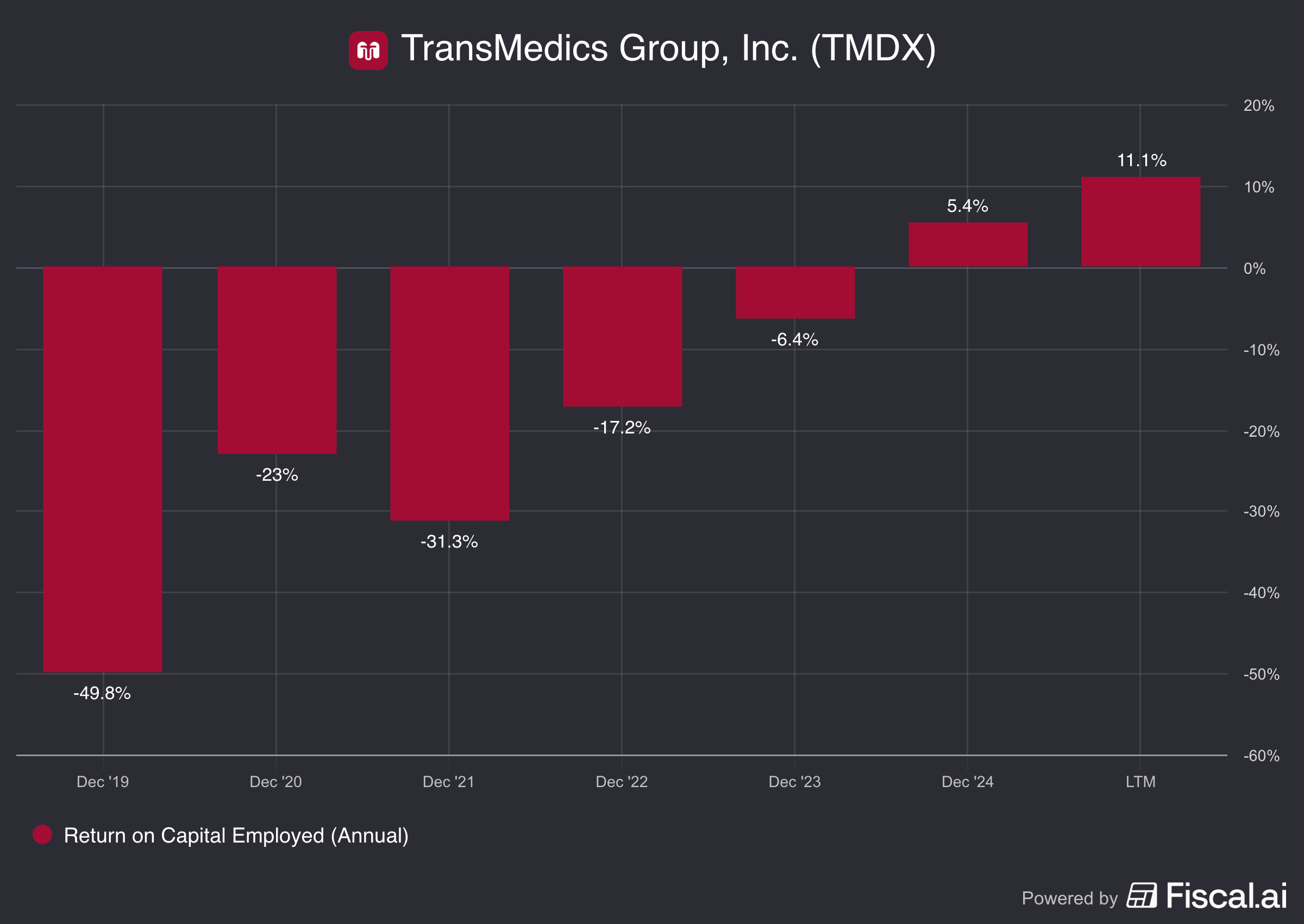

TransMedics has an average ROCE of -7% over the past 5 years, mainly due to having shortly achieved profitability. However, since this ratio has grown from -31% in 2021 to 11% in the last twelve months, we can expect for it to keep growing in the following years.

Having said that, since TransMedics is a highly specialized logistics company which owns over 21 planes, it would be surprising to see the company exceed our threshold of 15% for the long term.

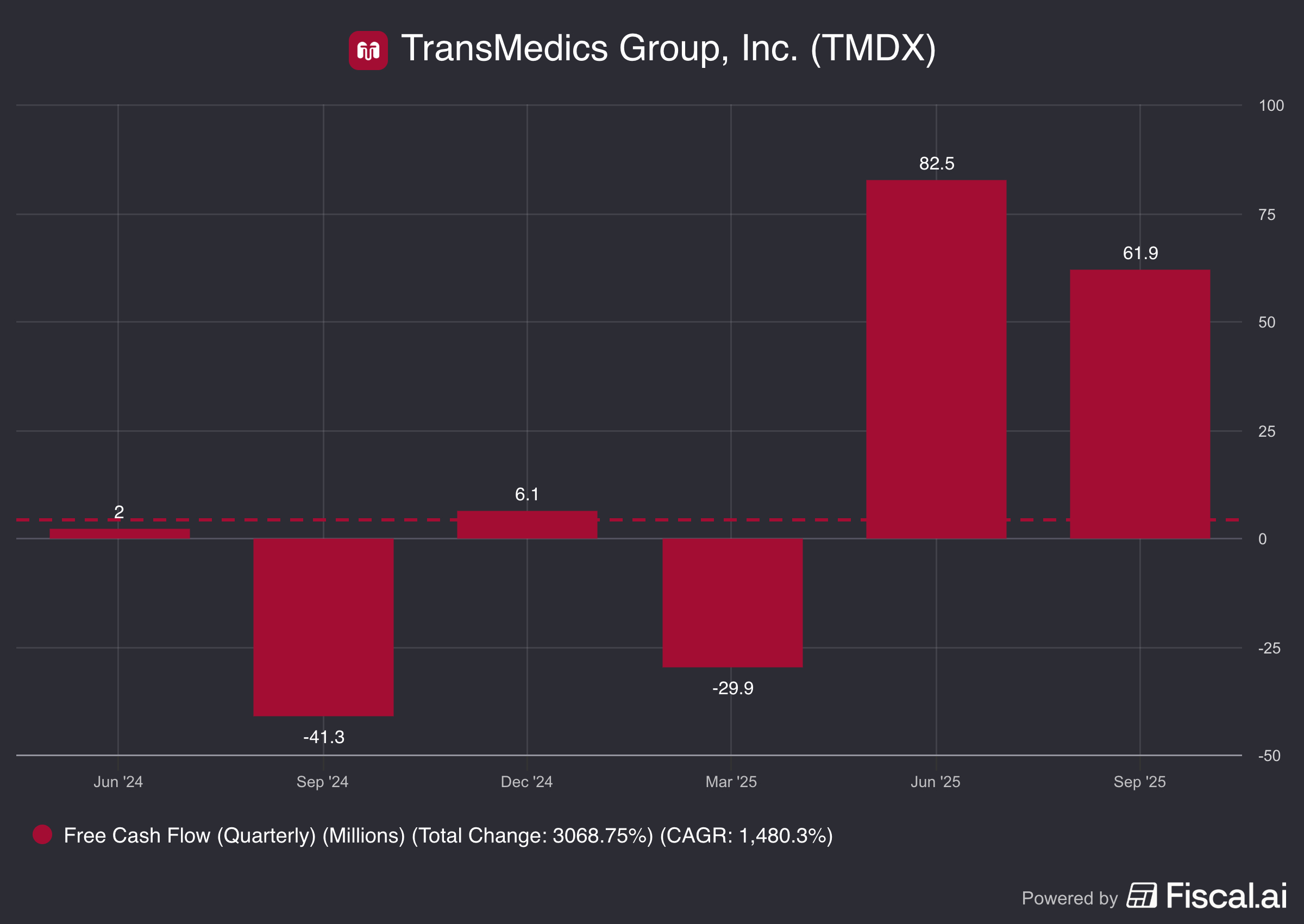

Free Cash Flow Consistency: (0/1)

TransMedics has not yet established a record of predictable and consistent FCF generation, as in the past 6 quarters it has had 2 quarters with negative FCF and 2 quarters with an FCF generation above $60 million. However, this could be attributed to the fact that the company just recently became FCF positive, and in the following quarters it could keep the FCF generation it delivered in the previous 2 quarters.

Resilience & Cyclicality: (1/1)

TMDX’s business is highly resilient to typical economic downturns as the demand for organ transplantation is driven by chronic illness and is not dependent on consumer spending. Organ transplants are life-saving, non-elective medical procedures which are primarily funded by Government programs and private insurance.

6. Growth and Profitability

Sustainable Double-Digit Growth: (1/1)

$TMDX is estimated to achieve revenues of $998 million in 2028 (TradingView). When considering that their revenues in 2024 were $442 million, this projection would indicate a 22.6% revenue growth CAGR, which is well above the double-digit growth we would expect to see.

Growth Levers: (1/1)

TransMedics has a clear plan for future expansion. The company's strategy can be divided into three main pillars:

Expanding the market by introducing the OCS platform into the the kidney transplant market.

Deepening the moat by investing heavily in R&D to improve transported organ health, solidifying its dominance and increasing utilization rates.

Expand geographically to high growth overseas markets like Italy and other European countries.

Pathway to Profitability: (2/2)

TransMedics turned profitable in early 2024 and has since been consistently expanding its margins.

7. Red Flags and Risks

Lack of an Economic Moat: (0/-2)

TransMedics currently has a wide moat due to its intangible assets, high switching costs, and large recurring customer base.

Balance Sheet Risk: (0/-2)

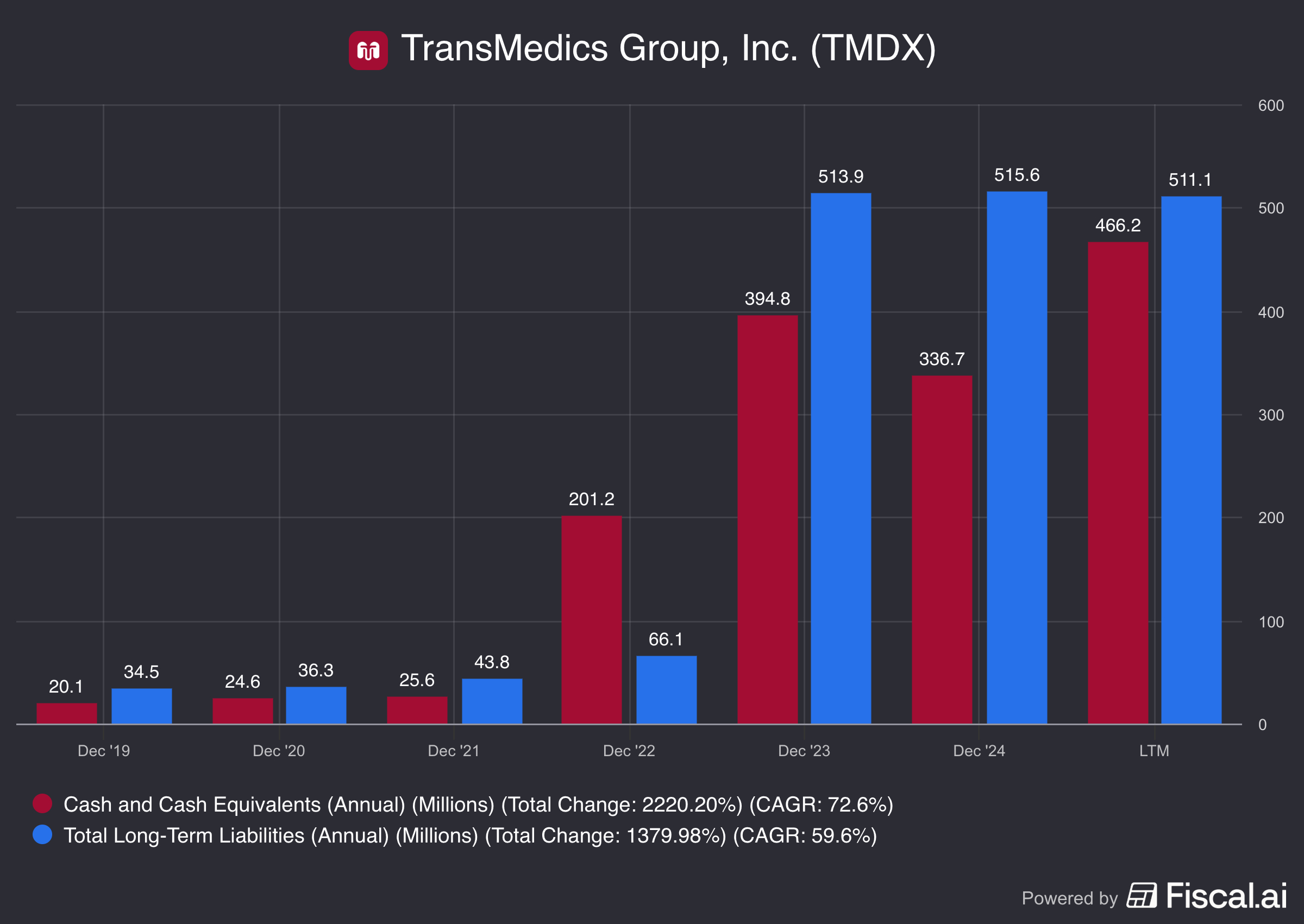

TransMedics' balance sheet is very solid. As of December 2025 its cash and cash equivalents were $466 million, while its total liabilities amounted to $511 million.

Lack of Profit Visibility: (0/-2)

TransMedics turned profitable in early 2024 and has since been consistently expanding its margins.

Regulatory & Geopolitical Risk: (-0.5/-1)

TransMedics is highly vulnerable to changes in domestic regulations, as its revenue is critically dependent on FDA regulation and reimbursement policies from Medicare, Medicaid, and private insurance. Any adverse change to approval requirements or payment rates could directly impact sales and margins.

On the other hand, the company’s core revenue is generated by NOP, which operates entirely within the US, providing resilience against geopolitical risks.

Core Business Disruption: (-0.5/-1)

Currently, TransMedics maintains a strong moat in the area of organ preservation and transportation due to its patented technology. However, the most significant long-term risk of total disruption lies in the scientific advancements of xenotransplantation (using genetically modified animal organs, like pig kidneys, currently in early human trials) or synthetic organs, which promise a future of organs created on demand, eliminating the need for organ preservation and transportation.

Customer Concentration Risk: (0/-1)

TransMedics does not have high customer concentration risk as stated in its 2024 annual report.

“For the years ended December 31, 2024 and 2023, no customer accounted for more than 10% of revenue.” - TransMedics’ 2024 Annual Report

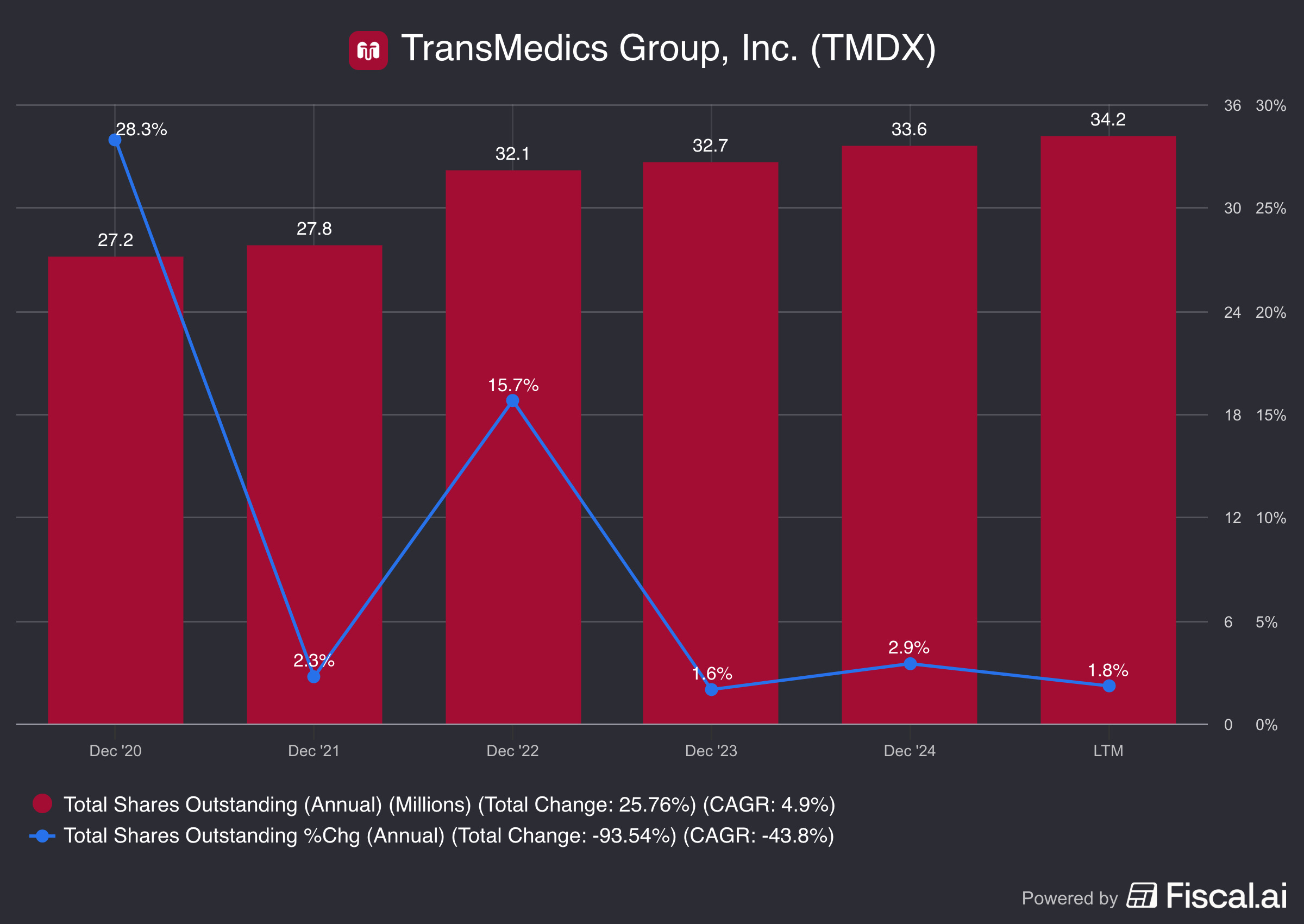

Share Dilution: (0/-1)

TransMedics’ total shares outstanding increased by 2.9% from 2023 to 2024, mainly caused due to its SBC, needed to retain top talent.

However, I believe that this dilution should not be a cause of concern for investors as EPS growth is much faster than its dilution.

TransMedics Group Quality Score (FINAL):

Adding up the scores and deducting one for potential risks, TransMedics scores a total of 15/22 points, making it a “Viable” business and one which does not deserve a Deep Dive analysis at the moment.

Despite TransMedics’ incredible value proposition and clear market leadership, I believe that the company is simply a highly specialized logistics company operating in a highly regulated industry.

Moving forward we will not be conducting further analysis on TransMedics ($TMDX) due to its fundamentals not meeting The Compounder Score’s strict criteria.

Follow to not miss out, it’s FREE!

We are currently prioritizing making these posts about as many companies as possible to give you the highest chance at identifying the right one for you. However, like this post or leave a comment since, the higher the engagement, the higher the likelihood of us conducting a Deep Dive on the company (as long as it is a “High Conviction” or a “Best-in-Class”).

Thanks for taking the time to read this post!

Best,

The Cash Flow Compounder

I am much more negative on TMDX. I think it's a low quality business that won't hit volume or margin targets due to competitive pressures that will emerge in the next few years. My reasons below:

1) Undifferentiated business model

The NOP model actually lowers stickiness and barriers to entry. Medical devices are typically "sticky" because hospital staff need to be trained, with multi-year contracts reinforcing product adoption. The NOP model of bundling service and product - streamlining the process to a simple phone call - eliminates switching costs and commoditizes the business model.

This would be fine if the technology was somehow differentiated, but it's not. This isn't complex tech at all. And there isn't evidence to show that that TMDX is superior to OrganOx, Liver Transport, or VitaSmart in liver viability ex-vivo. OrganOx got transport approval in September of last year. The CEO responded to this clear competitive threat by saying OrganOx can't compete in transport because their device "can't fit on a plane" (paraphrasing) Not kidding - google the device right now and see if you agree with this take.

I don't believe owning a fleet of planes is a differentiator. If the ROI is there, OrganOx will undertake the capex project, or just lease the planes. The whitespace is white enough for multiple players each with fleets.

Once TMDX starts getting competed against directly, the choice for customers quickly becomes “who gives me acceptable outcomes at the lowest cost with decent service,” especially given OrganOx is roughly one‑third the cost.

2) Unrealistic Volume Target

The 10,000‑organ target is very unrealistic. It leans heavily on DCD (donation after criculatory death) growth that would require uncontrolled DCD to work and be adopted at scale, which recent U.S. data and European experience don’t really support yet. It's a very novel idea. Beyond DCD, the Company also points to an opportunity in kidney transplantation, a lower-ASP market already dominated by LifePort, which has utilized perfusion technology for decades. This is also not to mention the negative tailwinds associated with kidney transplant volumes long-term (GLP-1s lowering incidence of diabetes - the primary reason for kidney transplantation)

3) NRP is a threat

Management likes to play up NMP (normothermic machine perfusion - the tech TMDX uses) vs cold storage. This is a strawman. The real argument is NMP vs NRP (normothermic regional perfusion).

NRP can cover multiple organs per run (and thus is usually cheaper on a per-organ basis). It also shows DCD outcomes comparable to DBD—often at a lower per‑organ cost.

While NRP is used at both the hospital and organ procurement organization (OPO) levels, TransMedics is structurally limited in its ability to compete with OPO-driven NRP solutions, as the company sells exclusively to hospitals.