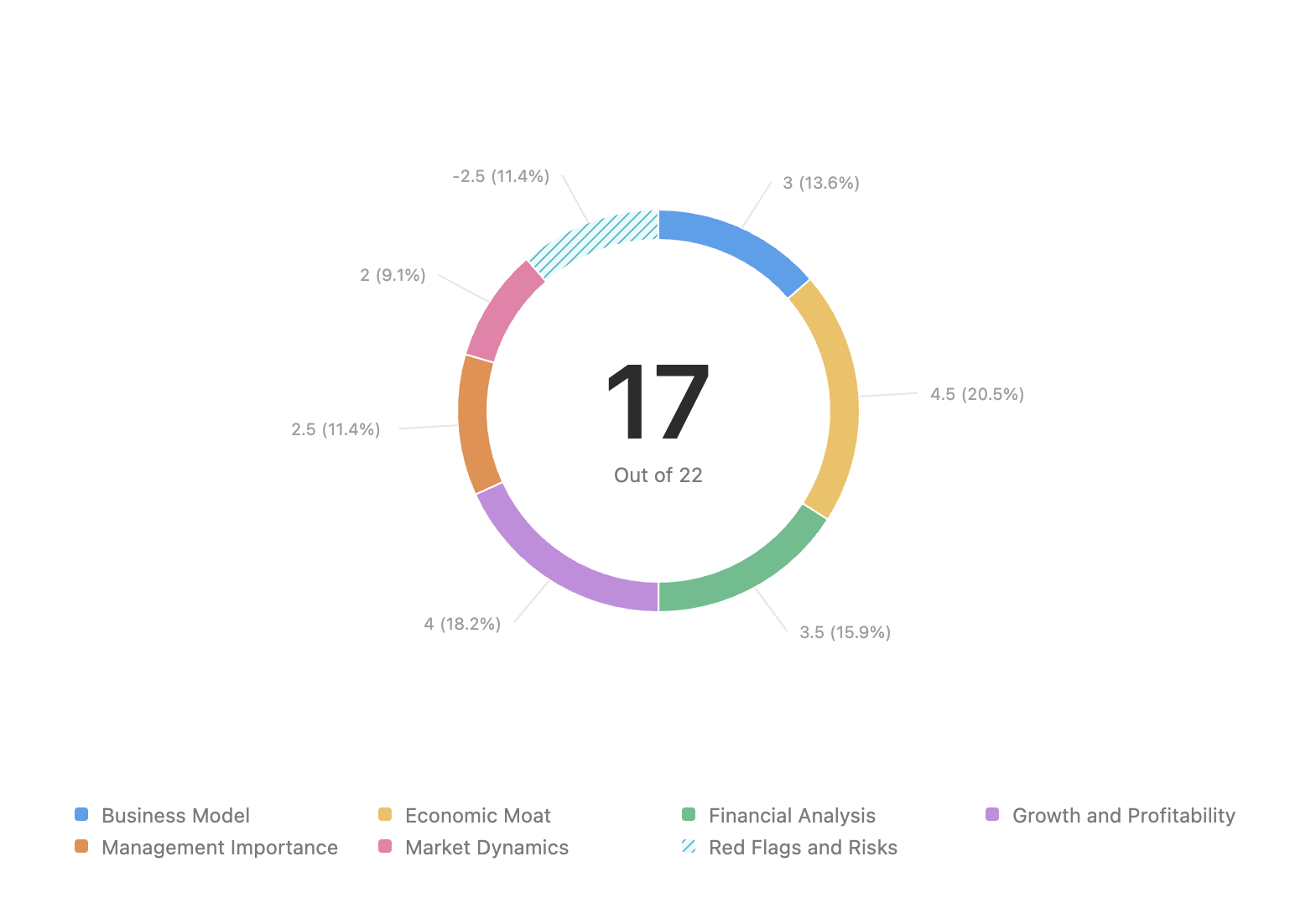

Camurus (The Compounder Score)

Mid-cap pharmaceutical company that has recently signed a +$900m contract with Eli Lilly

I applied The Compounder Score—a weighted framework for assessing companies’ fundamentals—as a preliminary screening tool to determine if Camurus ($CAMR.F) warrants a full deep-dive analysis.

The maximum score is 22 and the ranking system is as follows:

12 and below: High Risk/Pass

13 to 15: Viable

16 to 18: High Conviction

19 and above: Best-in-Class

The Compounder Score

Camurus is a pharmaceutical company focused on long-acting medicine for patients who struggle to stick to their recurring treatments.

Their target audience includes people with a wide range of conditions who must visit a clinic on a recurring basis to receive medication.

To battle these conditions, the company created its proprietary FluidCrystal® technology, which transforms daily pills into monthly injections, allowing patients to follow through with their treatments, generating better outcomes.

This drug delivery platform allows drugs to be injected as a liquid which slowly transforms into a gel, releasing the medicine over days or weeks.

The company’s two commercially approved products are Buvidal®, for opioid dependence, and Oczyesa®, for a rare hormonal disease called acromegaly.

What makes this company increasingly attractive is the recurring nature of its product, along with its growth potential through licensing deals with big pharmaceutical companies.

For example, recently Camurus entered into an agreement with Eli Lilly to become the exclusive provider for a long-lasting GLP-1 product which is under development.

Let’s analyze the company by using The Compounder Score:

1. Management Importance

“Skin in the Game” and Incentives: (2/2)

According to the company’s SimplyWallSt, individual insiders account for ~37.6% of the total ownership. This includes the stake from Sandberg Development, an investment company which funded Camurus’ creation in 1991.

Moreover, even though Fredrik Tiberg, the company’s Founder and CEO, only has ~2.8%, it represents ~$100 million. Since his company stock and options represent ~80% of his total yearly compensation, this could be classified as having significant Skin in the Game.

Business Resilience to Management: (0.5/1)

Since Camurus was founded in 1991, it has only had 1 CEO, Fredrik Tiberg.

Since Tiberg is also the company’s Chief Scientific Officer, he is involved in the strategic and scientific direction of the company’s pipeline.

A company like $CAMR.F, which is still in its early growth stage and has various products in its approval pipeline, is considerably dependent on its management.

However, since Buvidal operates independently due to its traction and licensing agreement with Braeburn, this may add a layer of resilience to management.

2. Market Dynamics

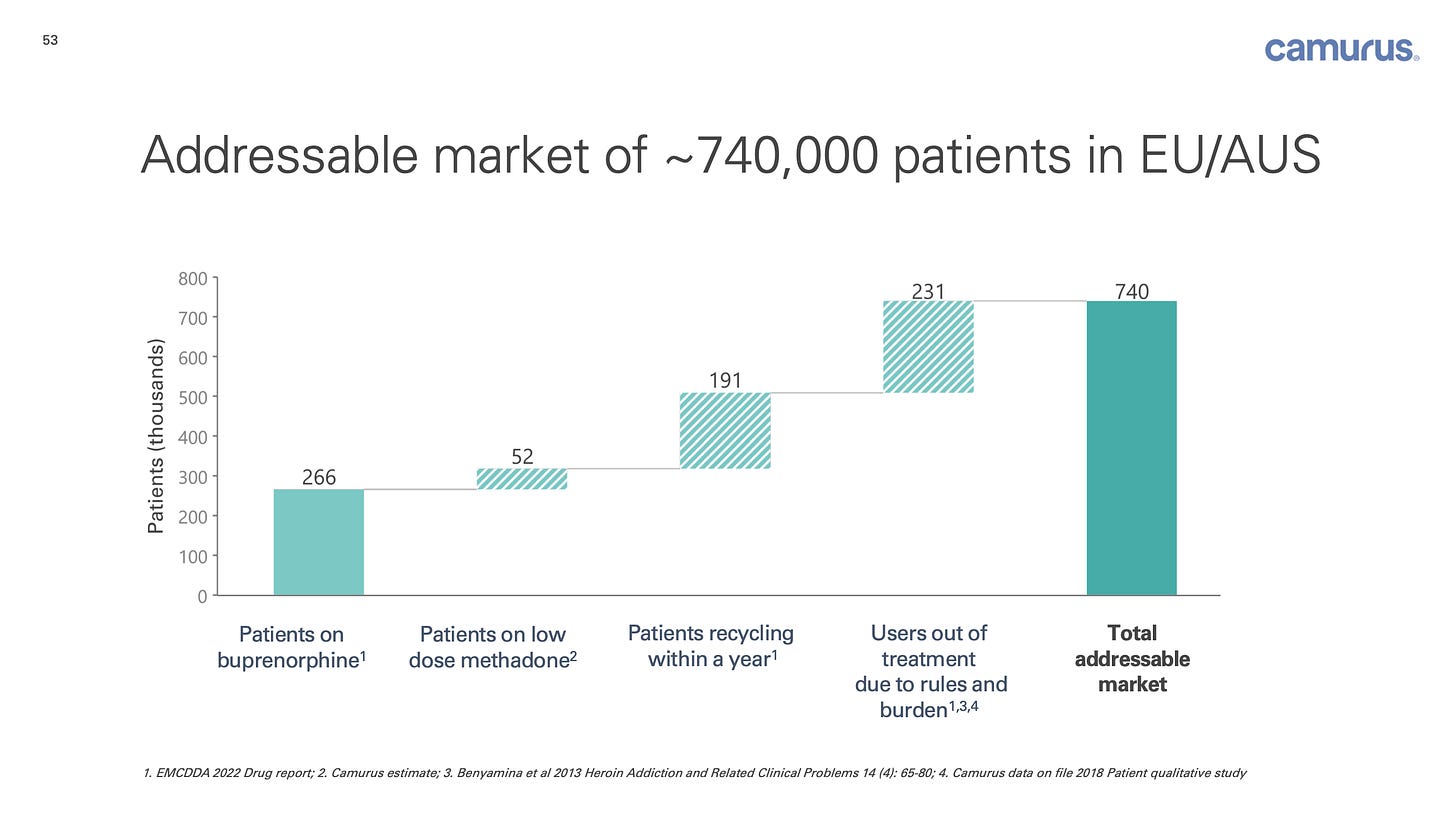

Large and Growing TAM: (1/1)

The most recent TAM estimation from Camurus appears in the company’s 2022 investors’ presentation.

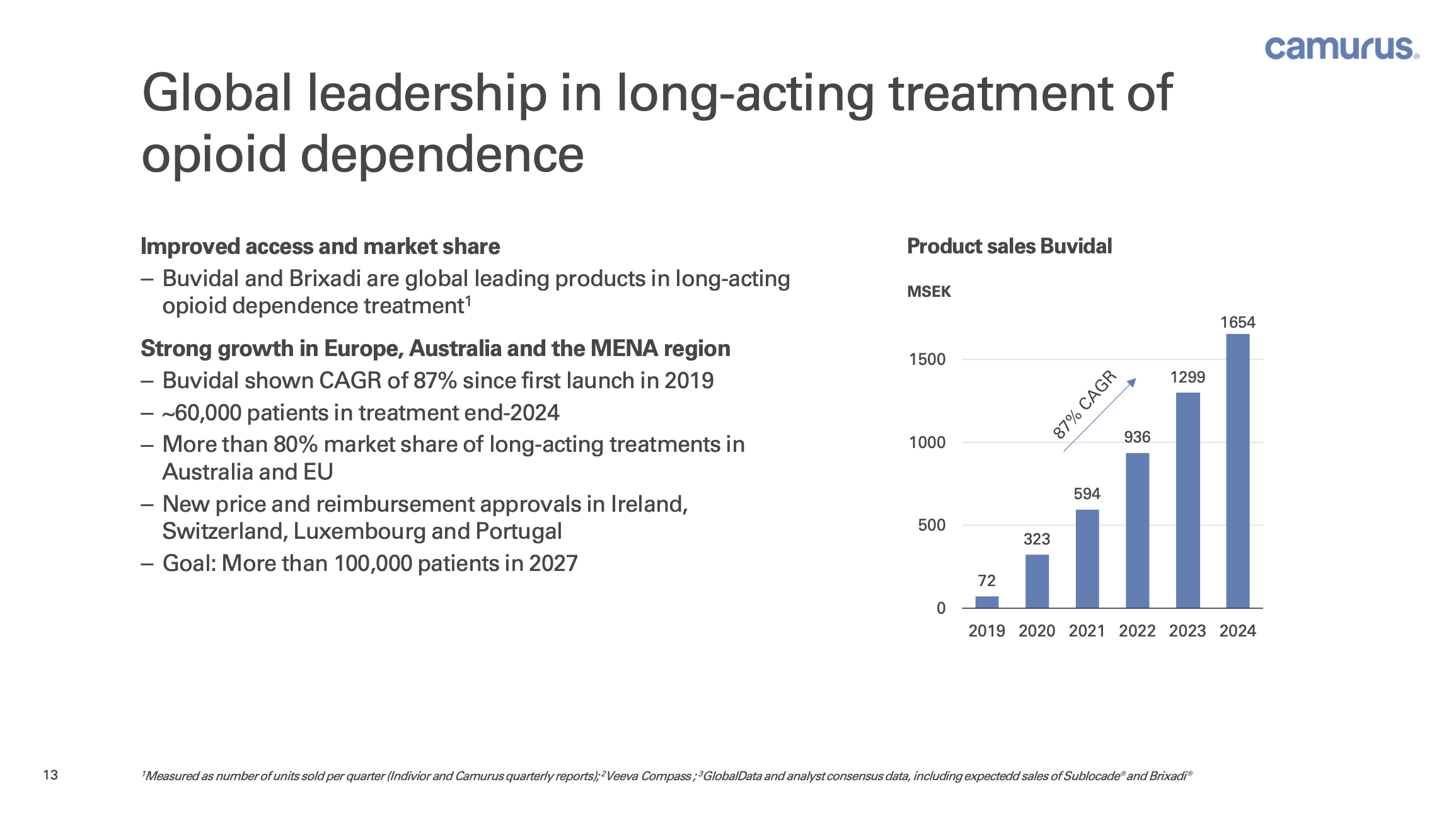

Here, the TAM for Buvidal is estimated at 740 million patients in the EU and Australia (the geographies where Buvidal was present at the time).

Camurus reported treating ~65,000 patients in June of 2025, with a goal of treating 100,000 patients in 2027, showcasing that there is significant room for future growth in its current segment for opioid treatment.

Additionally, since the company is expanding its portfolio through strong R&D, its TAM is expected to grow significantly as it enters the weight-loss and chronic pain segments.

Camurus - 2022 Investors’ Presentation

Exposure to Secular Trends: (1/1)

Camurus benefits from several powerful secular trends:

Global Opioid Crisis: The number of people suffering from opioid dependence keeps growing, driven by the overprescription of painkillers and the spread of synthetic opioids like fentanyl.

Long-Acting Treatments: Shifting away from daily pills toward long-acting, convenient formats like the FluidCrystal® technology.

Rare Disease Investment: Regulators are placing emphasis on rare diseases, speeding up approval pathways and market exclusivity.

Subcutaneous Drug Delivery: Increasing the treatments delivered via injection, allowing the platform to be applied to different compounds.

3. Business Model

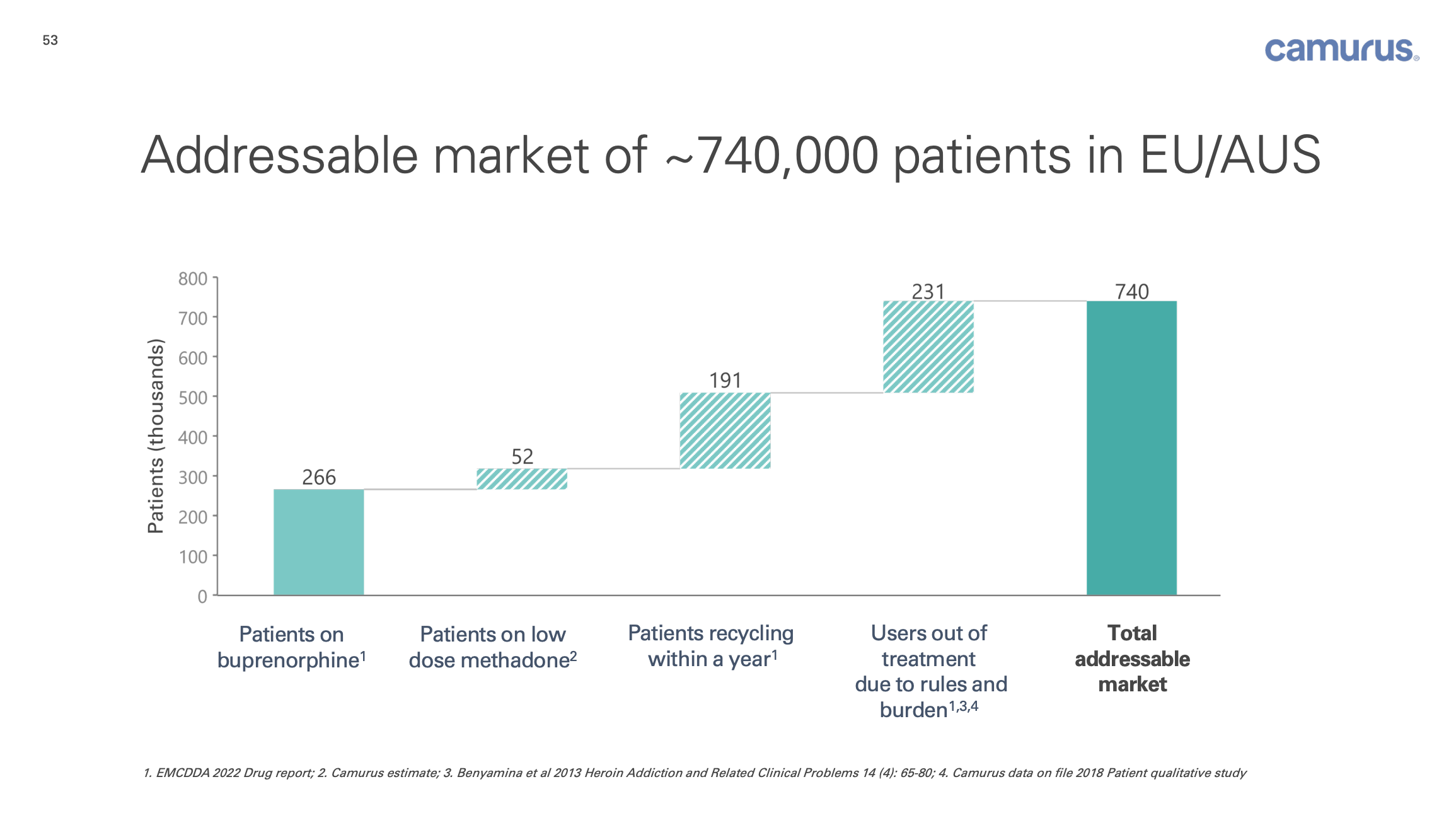

Asset-Light Model: (0/1)

Camurus had consistently maintained a CAPEX ratio below 3% of its revenue for the past 6 years, until 2025 where this ratio rose to 6.1%.

Moreover, due to being highly focused on top line growth, Camurus allocates a significant portion of its budget towards R&D and clinical trial costs, which in 2025 represented 22% of its revenues.

High Portion of Recurring Revenue: (1/1)

Since Camurus focuses on facilitating and simplifying long-term treatments, it has a high portion of recurring revenue:

Recurring Revenue (~88% of total revenues): Includes Buvidal product sales to healthcare providers where its patients require ongoing, continuous treatment. A typical opioid treatment lasts for months or years, creating a near-subscription-like revenue stream.

Royalties (~11% of total revenues): Since Camurus did not have a well-developed infrastructure in the US, it sold Brixadi’s commercial rights to Braeburns. From this agreement, the company receives royalties, which has a very similar profile to the company’s “Recurring Revenue” as it is the same product (sold under a different name).

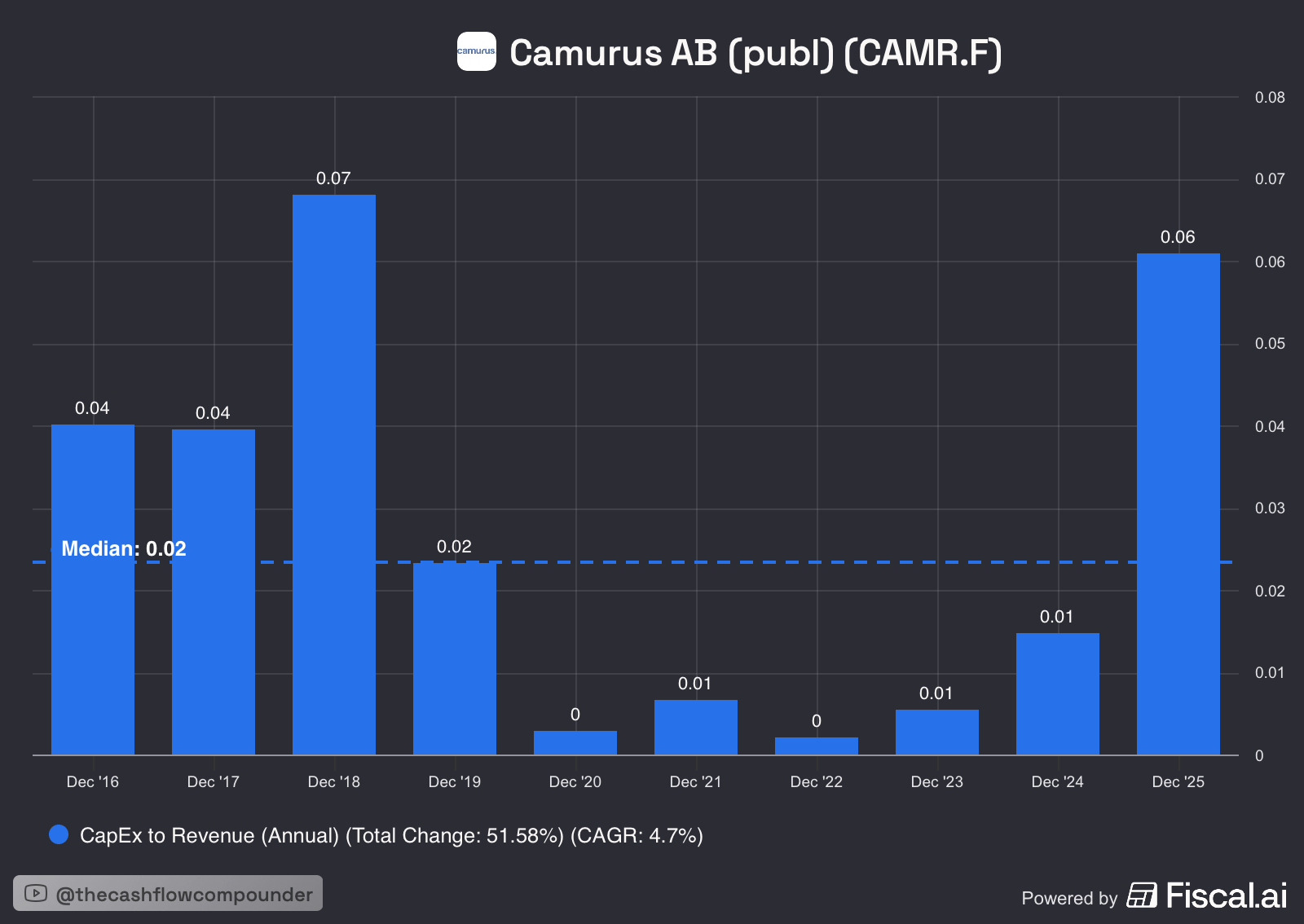

Margin Stability / Growth: (2/2)

Camurus’ margins have risen sharply since 2020, with the net margin expanding from -15.1% in 2021 to 32.5% in 2025.

The margin contraction experienced in 2024 is related to the one-time revenue related to the Brixadi US approval in 2023. Due to this milestone, Braeburn had to pay $35 million, which boosted the year’s net margin as it did not carry related COGS.

However, since then Camurus has continued to expand its net margin at a consistent basis.

4. Economic Moat

Sustainable Competitive Advantage: (2/2)

Camurus is mainly protected by its Intangible Assets.

The company has filed over 65 patents surrounding multiple aspects and features of its FluidCrystal platform, allowing to create a protection that is difficult to design around.

This is the hardest moat to replicate as competitors are legally banned from creating a product based on similar characteristics, allowing the company to be considered a monopoly for a limited time period.

Moreover, even if a competitor were to create a similar long-acting injectable technology, Camurus would still be protected via its exclusive agreement with Eli Lilly.

This, we predict will be one of the major revenue streams in the following years, as Lilly integrates it into its product line and Camurus searches for licensing deals in additional segments.

On our Hierarchical Level framework, Camurus achieves a Tier 3 (Structural Fortress) rating.

“If we were given the company’s entire market capitalization in cash (~$3 billion) to build a competitor, would it still be impossible to take their market share legally?” - Tier 3 Moat Litmus

This is the highest level of protection a business can possess, as no amount of money would allow investors to develop a similar solution to the FluidCrystal platform, or to enter the contract with Eli Lilly.

The company owns intellectual property and signed-agreements that are legally non-replicable.

Pricing Power: (0.5/1)

Camurus is able to increase its prices at a faster pace than inflation without losing customers for a sustained time period.

The main reason is that products for rare conditions like Buvidal and Brixadi face limited competition from other long-acting buprenorphine products.

However, the company will not be able to raise the take rate from its license agreements with Braeburn and Eli Lilly, where they are dependent on the price and volume increases from these companies.

Lastly, as pharmaceutical companies are highly regulated, significant price increases typically need to be validated by the main regulatory bodies to limit the monopolistic power which arises from the provided patents.

Dominant or Disruptive Position: (1/1)

Camurus is the clear global leader in the opioid dependence, long-acting treatment segment, with an estimated ~80% market share in Australia and the EU and ~25% in the US (Brixadi).

Embedded in Customer Behavior: (1/1)

Camurus’ treatments are deeply embedded in their customers’ lives as opioid dependence is a chronic condition which lasts for multiple months, years, or even indefinitely.

Additionally, switching between long-acting products is not common and these products have an incredibly low churn rate.

5. Financial Analysis

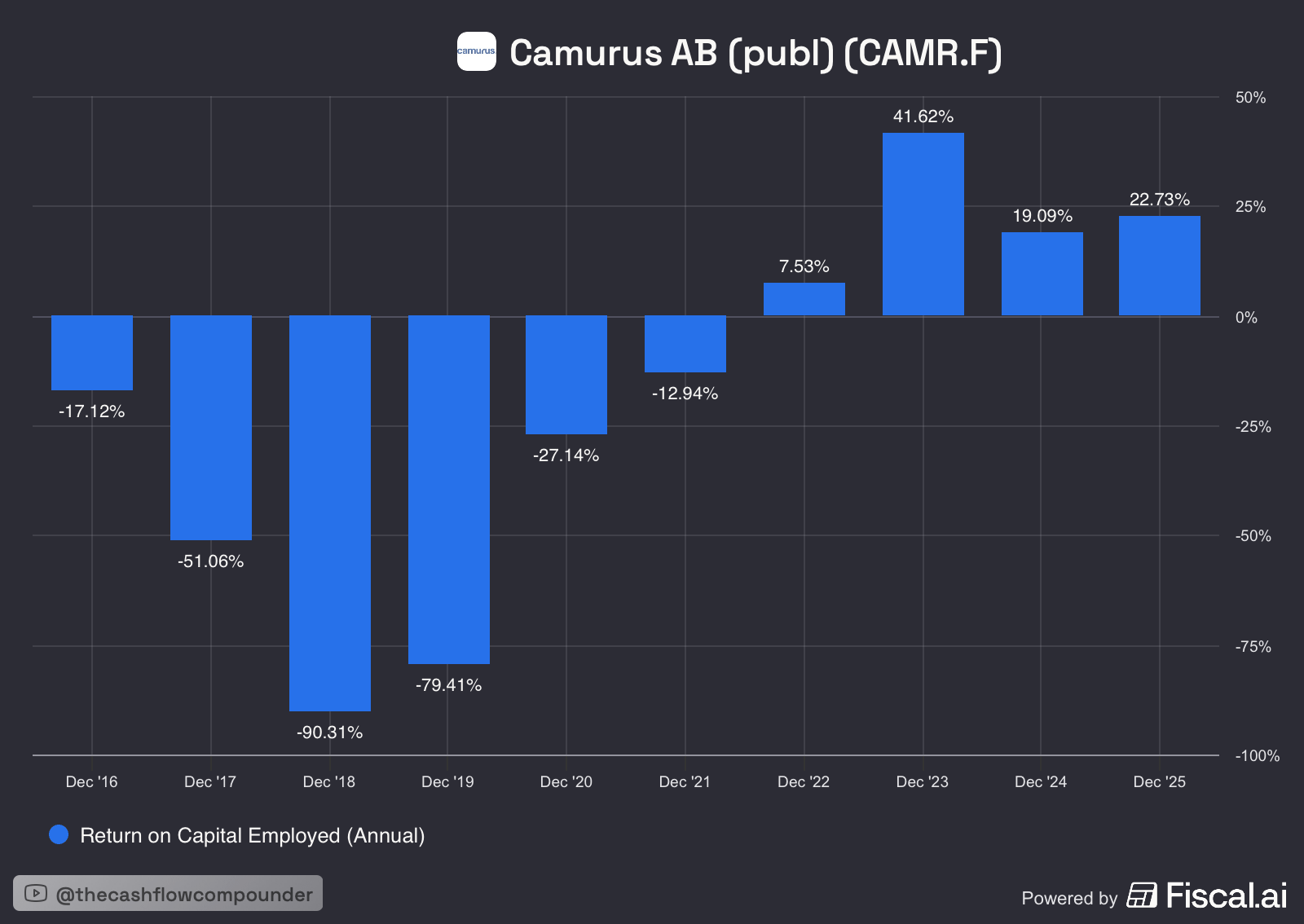

ROCE: (0/2)

$CAMR.F has an average ROCE of 19.4% over the past 5 years.

As stated previously, we can see that the ROCE achieved in 2023 is significantly larger than the following years (44.7%) due to the one-time revenue related to the Brixadi US approval in 2023.

Camurus’ ROCE has been above our threshold of 15% for the past 3 years, currently at a 22.7%, suggesting that the company creates significant value for shareholders as it is above a typical cost of capital, WACC.

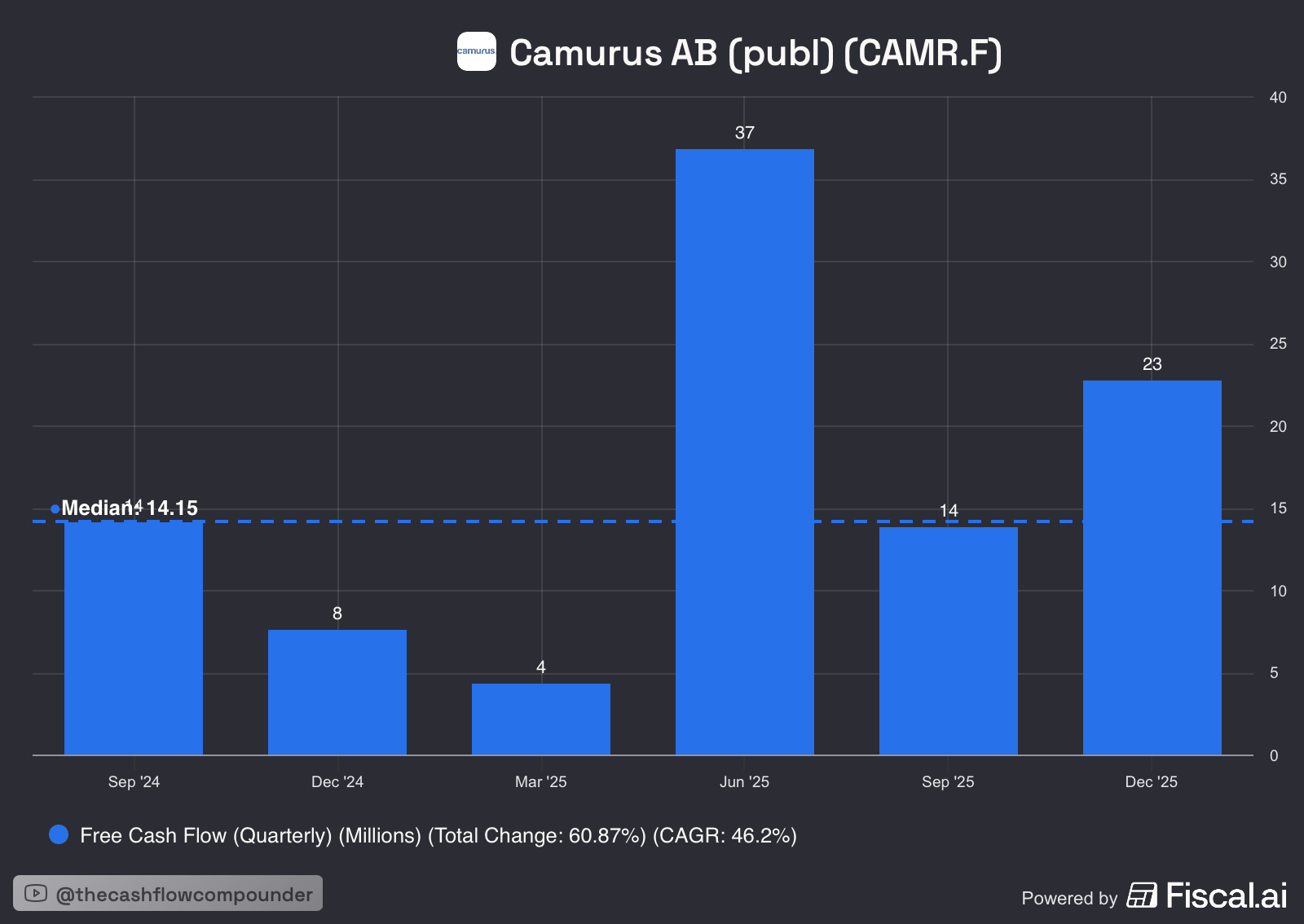

Free Cash Flow Consistency: (0.5/1)

Camurus has not established a record of predictable and consistent FCF generation, with high variance between the most recent quarters.

However, the company has been able to grow its FCF generation significantly in the past years, at a ~102% CAGR since 2021.

Resilience & Cyclicality: (1/1)

Camurus’ business model is highly resilient as its patients with severe, chronic diseases like opioid dependence will maintain their treatments even when the economy is weak.

Government funding for addiction treatment has typically been maintained or even increased during downturns, as the costs of untreated addiction become more visible during economic recessions.

6. Growth and Profitability

Sustainable Double-Digit Growth: (1/1)

Camurus is estimated to achieve revenues of ~$890 million in 2029 (TradingView).

When considering that their revenues in 2025 were $246 million, this indicates a ~39.0% revenue growth CAGR.

This estimated growth is much higher than the double-digit growth we expect to see.

Growth Levers: (1/1)

Camurus has individual levers for growth. The company's most important strategic areas are:

US Market Penetration: Brixadi achieved a ~39% market share just 15 months after its launch in the US, the largest opioid treatment market in the world.

Launch of Oczyesa for Acromegaly: The EU granted authorization for Oczyesa for acromegaly treatment in June 2025 and FDA approval in the US is currently being pursued.

Oczyesa for GEP-NET and PLD: Oczyesa is being evaluated for treating additional rare diseases, GEP-NET and PLD, which could double or triple the revenue opportunity.

Eli Lilly Agreement: This gives Eli Lilly the exclusive license to develop long-acting weight loss and metabolic disease drugs, which have shown faster and greater body weight reductions than Wegovy®.

Pathway to Profitability: (2/2)

Camurus has been profitable since the 2022 and has since been expanding its margins.

7. Red Flags and Risks

Lack of an Economic Moat: (0/-2)

Camurus has a Tier 3 (Structural Fortress) rating based on its strong intangible assets.

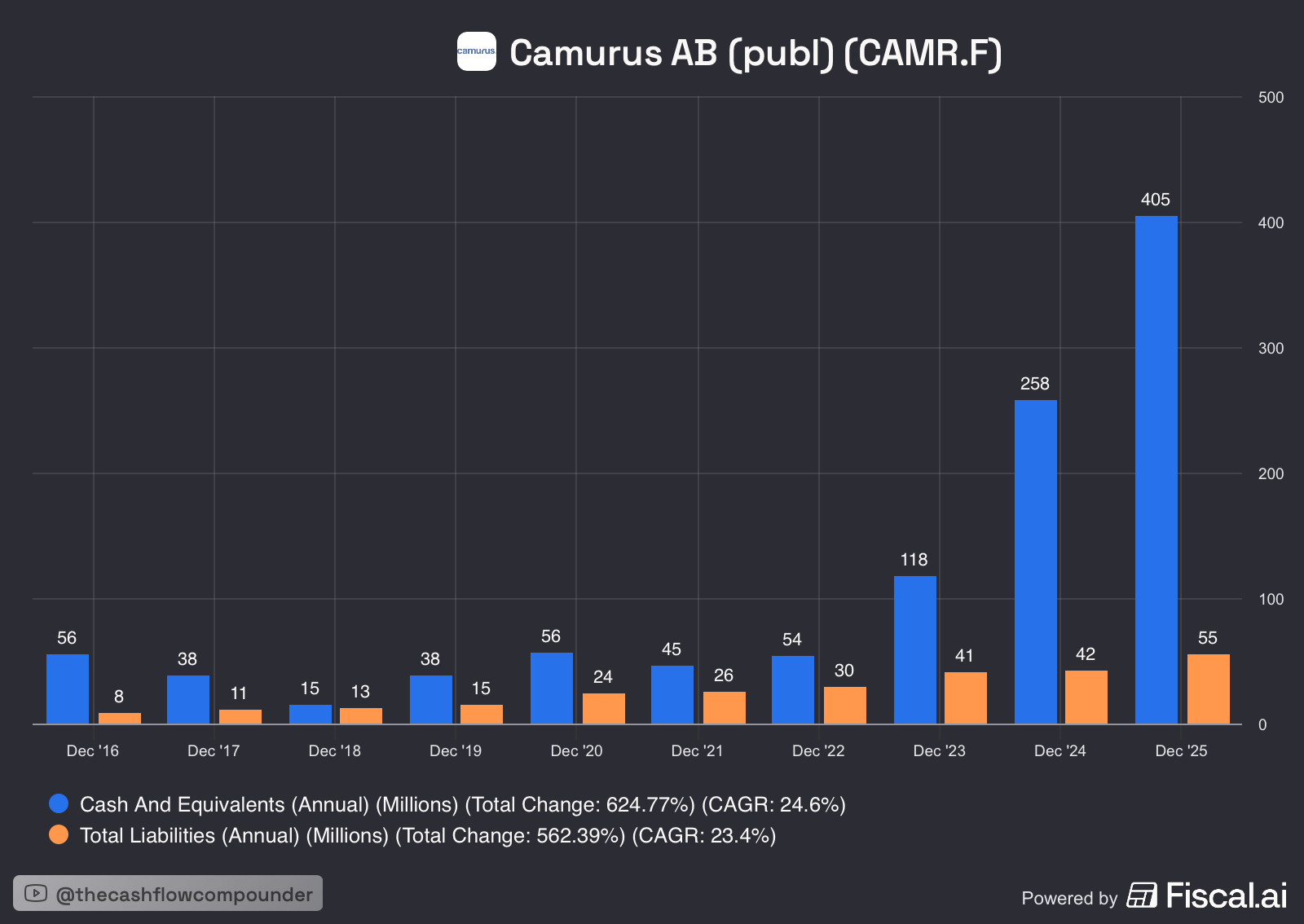

Balance Sheet Risk: (0/-2)

Camurus’ balance sheet is incredibly solid. As of April 2026 its cash & cash equivalents were $405 million, while its total liabilities amounted to $55 million.

After seeing the explosive growth of the company’s cash & cash equivalents over the past 2 years, the rising ROCE becomes even more impressive, as a larger asset base acts as downward pressure on capital efficiency ratios.

Lack of Profit Visibility: (0/-2)

Camurus has been profitable since the 2022 and has since been expanding its margins.

Regulatory & Geopolitical Risk: (-1/-1)

As Camurus is a pharmaceutical company, it is highly sensitive to regulatory risks which may complicate new project development or limit price increases for Buvidal and Brixadi.

Despite this being inherent in the sector, it does remind investors that a big part of the company’s future success is dependent on external factors.

Despite Camurus operating in stable, well-regulated markets like Europe, the US, and Australia, it is still exposed to significant currency risk as it reports in SEK but sells its product in USD, EUR, AUD, and other smaller currencies.

Core Business Disruption: (-0.5/-1)

Pharmaceutical companies must continue to innovate constantly to maintain their leadership position as competitors may develop a superior long-acting formulations or alternatives to Camurus’ existing products.

Additionally, despite the company’s patented long-acting technology, the high dependence it has on Buvidal increases its disruption risk as we have seen with prior investments like Lantheus Holdings.

This company also had a superior, patented product which represented most of its revenue. However, the company’s stock lost over 50% of its value as a competitor launched a cheaper alternative.

Customer Concentration Risk: (-0.5/-1)

Although Camurus’ products are sold to thousands of customers it’s concentration risk is expected to increase in the following years.

On the one hand, all commercial activity in the US flows through a single partner, Braeburn Pharmaceuticals.

On the other hand, the company is expected to experience a significant portion of its growth from its agreement with Eli Lilly.

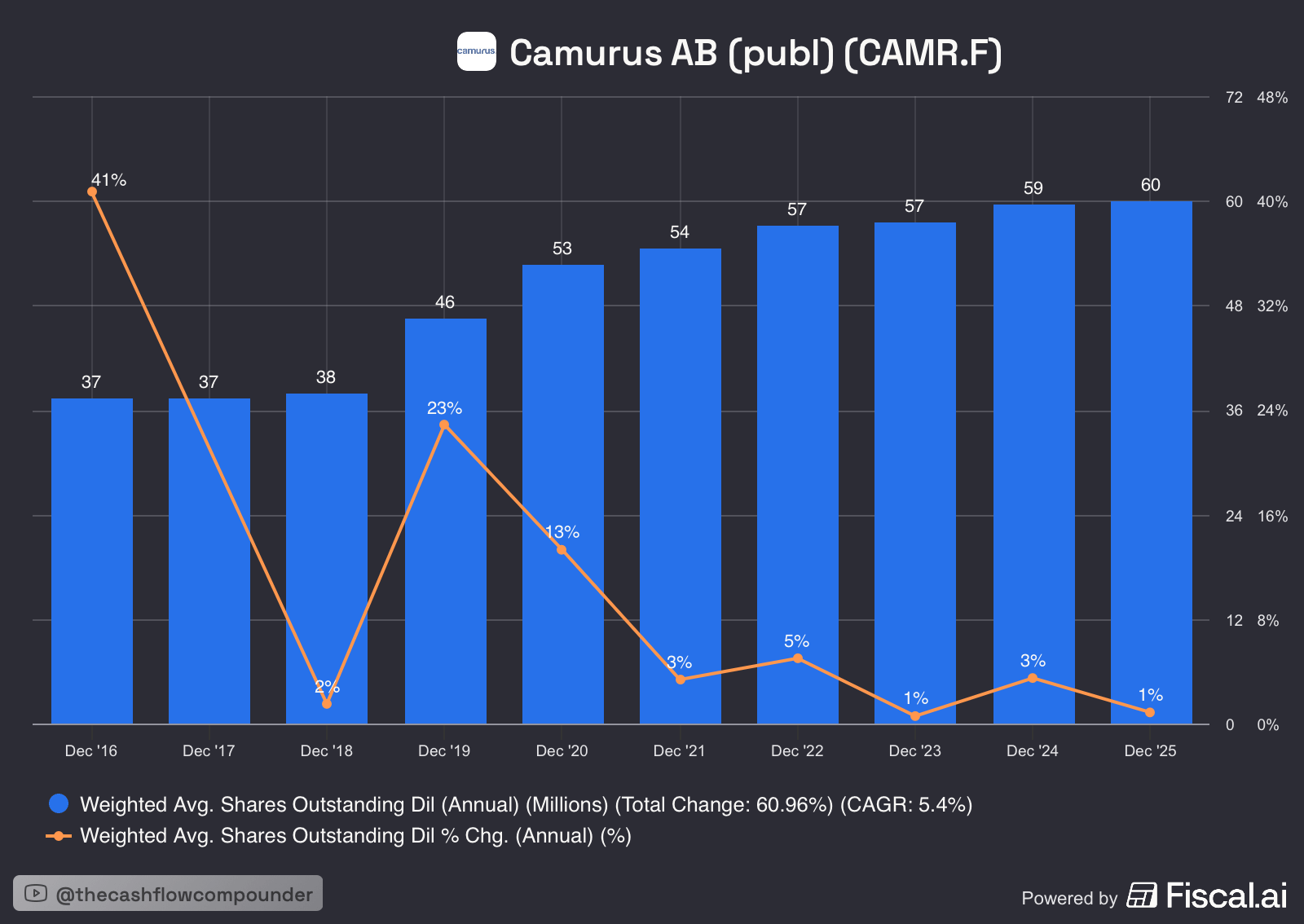

Share Dilution: (-0.5/-1)

Camurus’ total shares outstanding increased by 0.9% from 2024 to 2025 and the company has been issuing shares every year through its stock-based compensation schemes.

In the past 5 years, its share count has increased by ~14%.

Camurus Quality Score (FINAL):

Adding up the scores and deducting one for potential risk, Camurus scores a total of 17/22 points, making it a “High-Conviction” business.

Please leave a like if you enjoyed this post and found it valuable!

We have reviewed Camurus’ fundamentals utilizing our proprietary framework, The Compounder Score.

However, does this mean that the stock is trading at a valuation where it should be deemed a clear buy or is the risk too high?

The final, essential sections cover:

Comparable Analysis of Camurus’ historic valuation ratios versus its peers.

The Compounder DCF with potential return and intrinsic value estimates based on scenarios.

This part of the analysis is reserved exclusively for our premium subscribers to reward for their amazing support.

Subscribe now to get full access to all our upcoming analyses!

Camurus’ Valuation: