Adobe (The Compounder Score)

The creative powerhouse which has been severely punished by the market...

I applied The Compounder Score—a weighted framework for assessing companies’ fundamentals—as a preliminary screening tool to determine if Adobe ($ADBE) warrants a full deep-dive analysis.

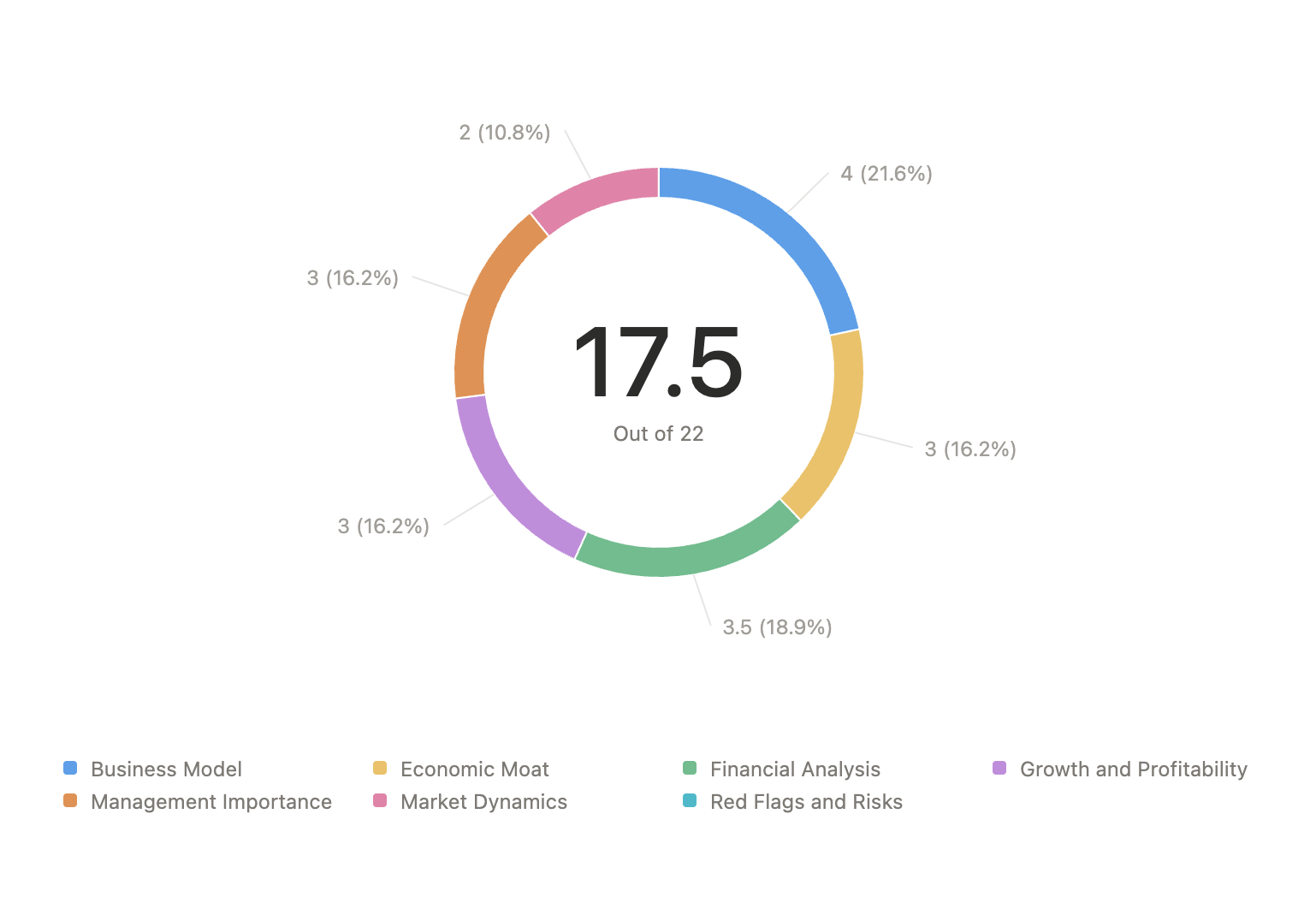

The maximum score is 22 and the ranking system is as follows:

12 and below: High Risk/Pass

13 to 15: Viable

16 to 18: High Conviction

19 and above: Best-in-Class

The Compounder Score

Adobe is the worlds largest creative provider, allowing anyone, from a teenager making a TikTok video to a professional filmmaker at a major studio, to bring their ideas to life. In 2025, Adobe reported that 99% of Fortune 100 companies have used AI features within an Adobe application, showcasing their impressive reach.

The company follows a SaaS model, allowing its customers to pay a monthly or yearly subscription to access their software. Despite the company’s impressive presence within corporations, it also offers its solutions to individual entrepreneurs and students.

For an investor, Adobe is an attractive business model because it possesses a “natural monopoly” in many of its markets, as once a professional learns how to use Photoshop, they are unlikely to switch to a competitor. The company’s impressive FCF generation, combined with the market’s fear of an AI disruption has allowed Adobe to conduct record-breaking share repurchases, indicating management’s confidence in its business model and long-term success.

Let’s analyze the company by using The Compounder Score:

1. Management Importance

“Skin in the Game” and Incentives: (2/2)

According to the company’s 2025 Proxy Statement, individual insiders account for 0.17% of the total ownership in the company. Despite this being a relatively small percentage, since it represents over $235 million, it represents that management has significant “Skin in the Game”.

Additionally, the CEO and other NEOs received over 85% of their total 2024 compensation from stock awards, underlining the effort made by the company to align its management’ interests to its shareholders.

Business Resilience to Management: (1/1)

Since Adobe was founded in 1982, it has had three CEOs, John Warnock, Bruce Chizen, and Shantanu Narayen.

The successful transition between CEOs without operational disruption has shown that the business is resilient enough to survive a total change in leadership style. Since Adobe’s products are integrated so deeply into industry workflows, the company could likely continue to succeed even under average leadership.

2. Market Dynamics

Large and Growing TAM: (1/1)

Adobe operates in an incredibly large market, which it estimated at $205 billion in 2024, with the potential to grow to $293 billion in 2027.

This growth is expected to be fueled by the company’s introduction of new offerings and the expansion of multi-cloud, integrated solutions for enterprise customers.

Exposure to Secular Trends: (1/1)

Adobe’s offerings benefit from several powerful secular trends:

The Creator Economy: Millions are now making money through social media, requiring professional-grade editing tools to stand out.

Generative AI Integration: Adobe’s Firefly AI allows users to create images with simple text prompts, making high-end design accessible to anyone.

Personalization at Scale: Businesses want to show every customer tailored ads and websites, requiring massive data and enterprise-level marketing tools.

Remote & Hybrid Work: As teams work from different locations, the need for cloud-based collaboration tools has become permanent.

3. Business Model

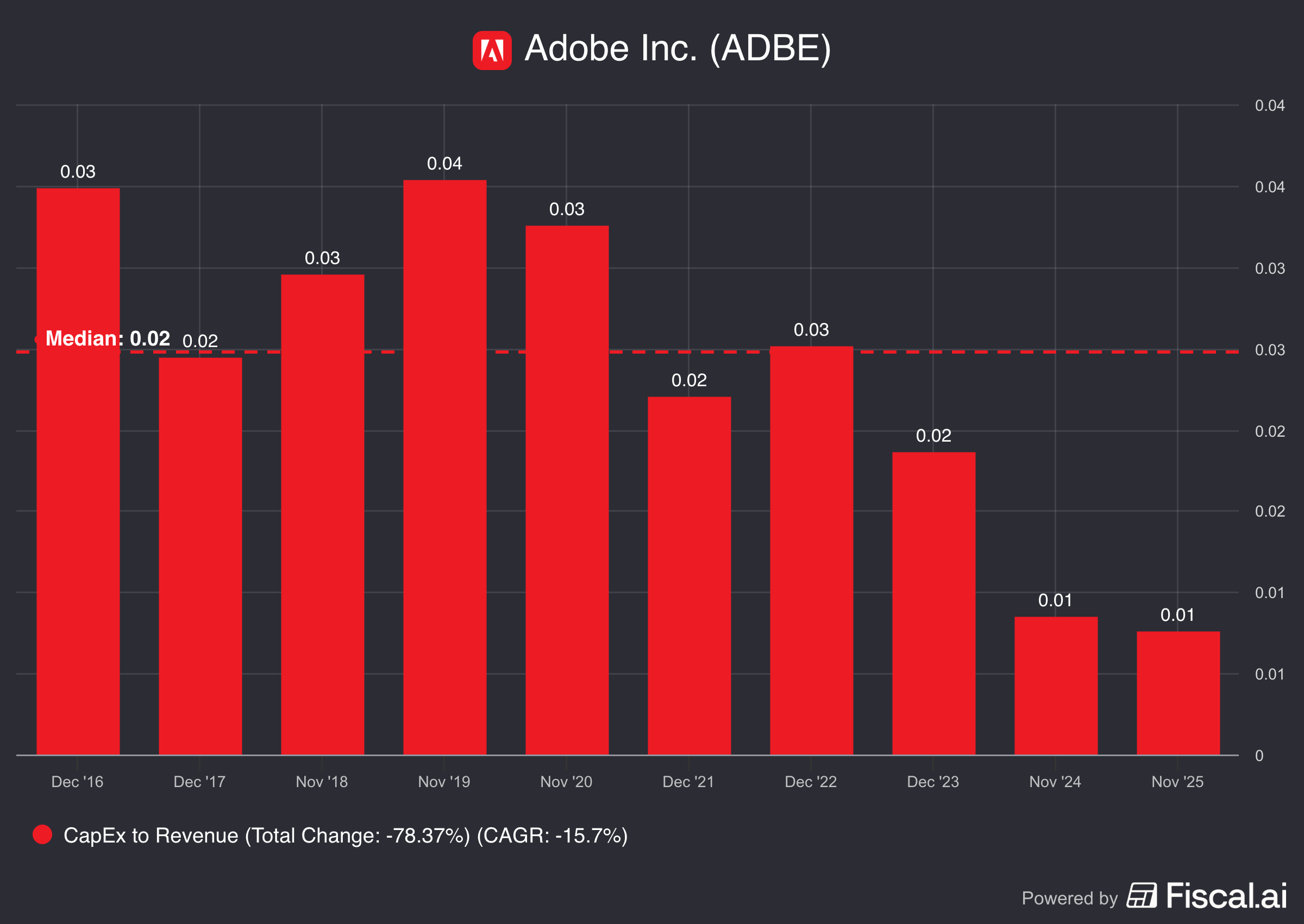

Asset-Light Model: (1/1)

Adobe has consistently maintained a CAPEX ratio of under 4% of its revenue for the past 10 years, with a 10-year median of 2%, allowing them to be considered an asset-light business.

High Portion of Recurring Revenue: (1/1)

Adobe’s entire SaaS model is based on recurring revenue, with approximately 97% of its revenue coming from subscriptions. This creates a highly predictable cash flow, allowing the company to focus on its long-term strategy rather than its day-to-day operations.

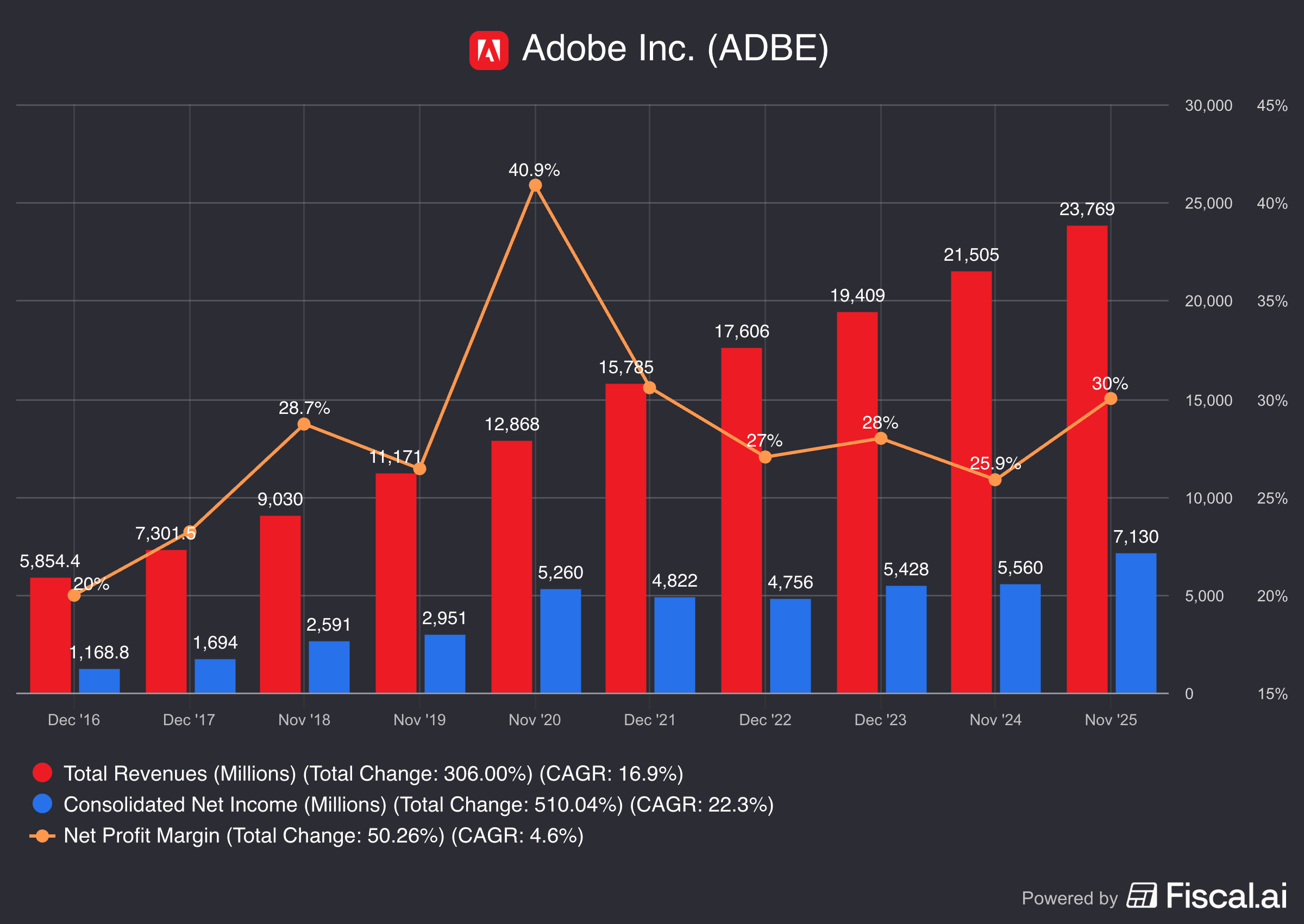

Margin Stability / Growth: (2/2)

Adobe’s margins have been expanding consistently, with the net margin rising from 27% in 2022 to 30% in 2025.

Despite not providing a long-term outlook for their profitability targets, we can see that management has been focusing on improving efficiency to optimize the value it generates for investors.

4. Economic Moat

Sustainable Competitive Advantage: (1/2)

ADBE 0.00%↑ has developed a moat which has been narrowed by AI, mainly based on its high switching costs and intangible assets.

Currently Adobe is deeply embedded in its customers’ workflows, as its Creative Cloud has become an operating system for creative production. Switching providers would require migrating all a company’s cloud assets, redesigning automation pipelines, and retraining thousands of employees.

On the other hand, Adobe’s moat is reinforced by its massive brand equity and IP, which has for example allowed Adobe’s Firefly AI to be trained on licensed Adobe Stock images, a massive intangible asset for Fortune 500 companies that are terrified of copyright lawsuits by other tools such as ChatGPT’s Sora.

Pricing Power: (0.5/1)

Adobe has been able to increase its prices at a faster pace than inflation without losing customers due to its tools being essential for the livelihood of creative professionals.

In the past, Adobe has raised its subscription prices by 5–10% every few years without losing a significant number of customers, as for a professional, an extra $5 a month is a small price to pay to keep the tools they use for 8 hours a day.

However, this is one of the main factors which is being affected by AI, as a lot of the smaller professionals are resorting to much cheaper, lower quality tools which can help them develop the content they need.

Dominant or Disruptive Position: (0.5/1)

Adobe is the clear dominant leader in the Creative and Document software markets. While AI companies like OpenAI's Sora could be seen as disruptive, Adobe has quickly integrated these technologies into its own apps, effectively “disrupting itself” to stay in the lead.

However, the market is currently filled with companies which are creating platforms which make “good enough” design accessible to everyone. Whereas you would need to spend months learning Photoshop to create a professional image, now you can type a prompt.

Embedded in Customer Behavior: (1/1)

For most of its users, Adobe has become a “need-to-have” platform. Its incredible distribution among the top universities worldwide has allowed it to become the standard toolset, meaning that students are “embedded” into the ecosystem before they even start their careers.

This is then very hard to change as they will have learned most their editing skills using Adobe’s products and in the event of switching providers, would have to learn the “pro-tips” from scratch.

5. Financial Analysis

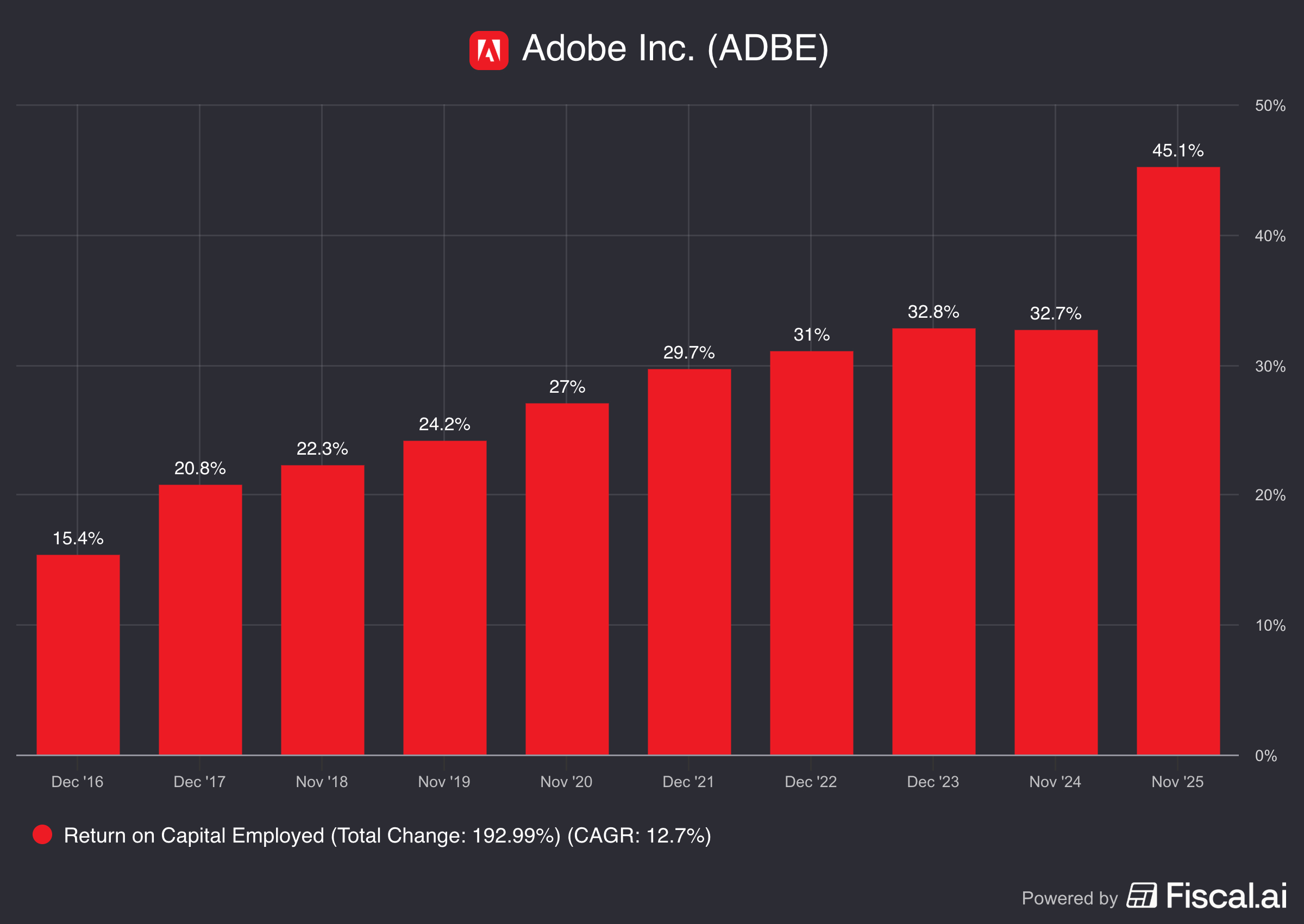

ROCE: (2/2)

Adobe has an average ROCE of 36% over the past 5 years, which has grown from 15% in 2016 to 45% in 2025.

Adobe’s ROCE has remained above our 15% threshold for the past 1'0 years, which implies that the company is able to create massive amounts of value for shareholders.

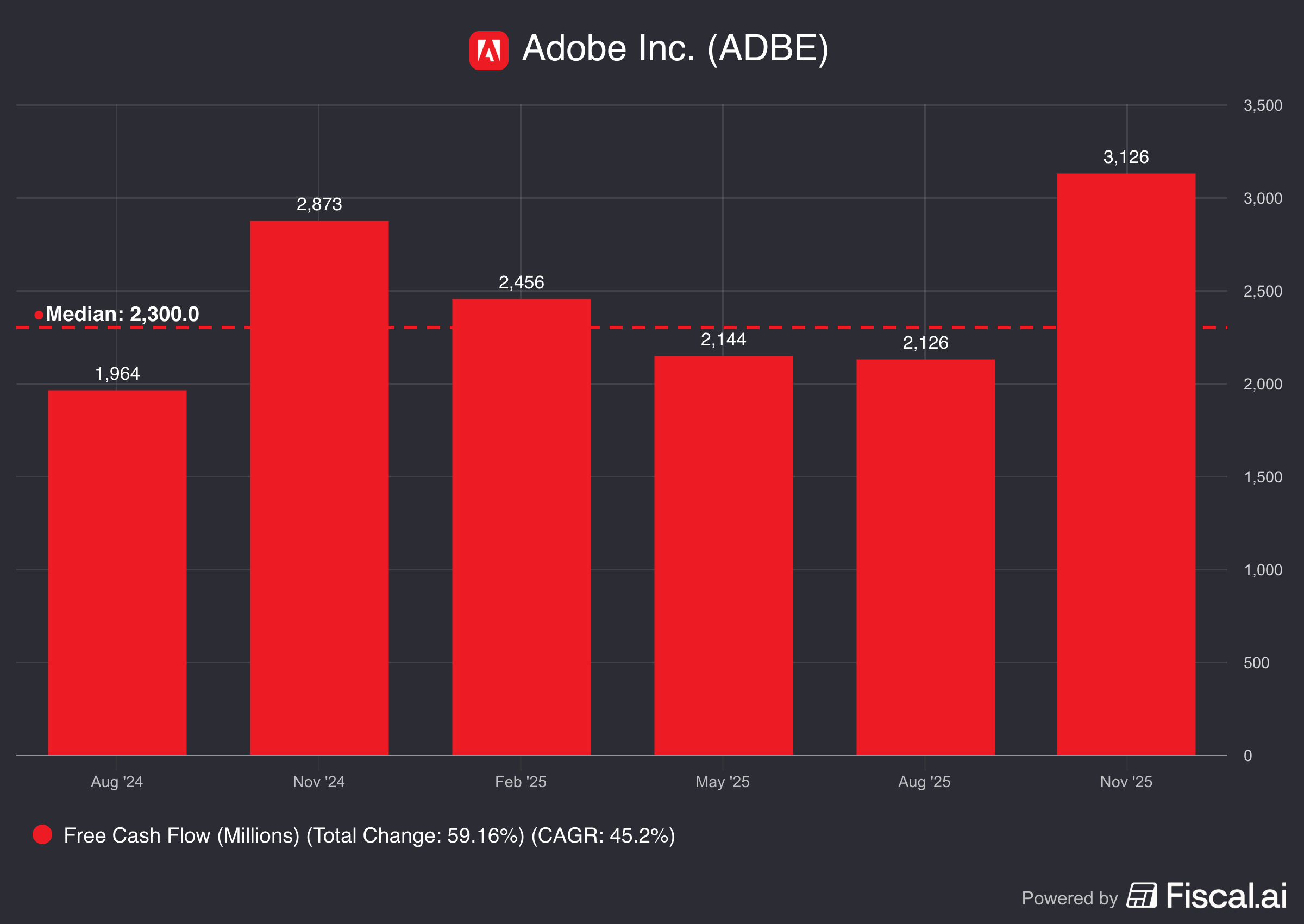

Free Cash Flow Consistency: (1/1)

Adobe is widely perceived as a consistency machine due to its ability to generate predictable FCF, which is growing at a great pace. This consistency is evident as most of their quarterly results are close to the period’s median of $2.3 billion. This is something we look for when researching companies as it reduces investment risk and supports higher valuation multiples for the stock.

Resilience & Cyclicality: (0.5/1)

Adobe enjoys a highly resilient business model. During economic downturns, individuals and businesses might cut back on new cars or travel, but they rarely cancel the subscriptions needed to do their jobs.

However, since marketing expenditure is widely perceived as highly cyclical, due to reductions in advertising budgets during recessions, most companies may reduce their number of “seats” when their margins are pressured.

6. Growth and Profitability

Sustainable Double-Digit Growth: (0/1)

ADBE 0.00%↑ is estimated to achieve revenues of $33.6 billion in 2029 (TradingView). When considering that their revenues in 2025 were $23.8 billion, this projection would indicate a 9.1% revenue growth CAGR, which is just under the double-digit growth we would expect to see.

Growth Levers: (1/1)

Adobe has a clear plan for future expansion. The company's most important strategic areas are:

Firefly AI Monetization: Charging extra for “AI credits” as users generate more images and videos using Adobe’s AI tools.

Expanding Document Cloud: Pushing Acrobat and e-signatures into businesses that are still using old-fashioned paper.

Acquisitions: Using its massive cash flow to buy smaller, innovative companies to add new features.

Mobile Apps: Creating simpler versions of their tools to capture the millions of casual creators.

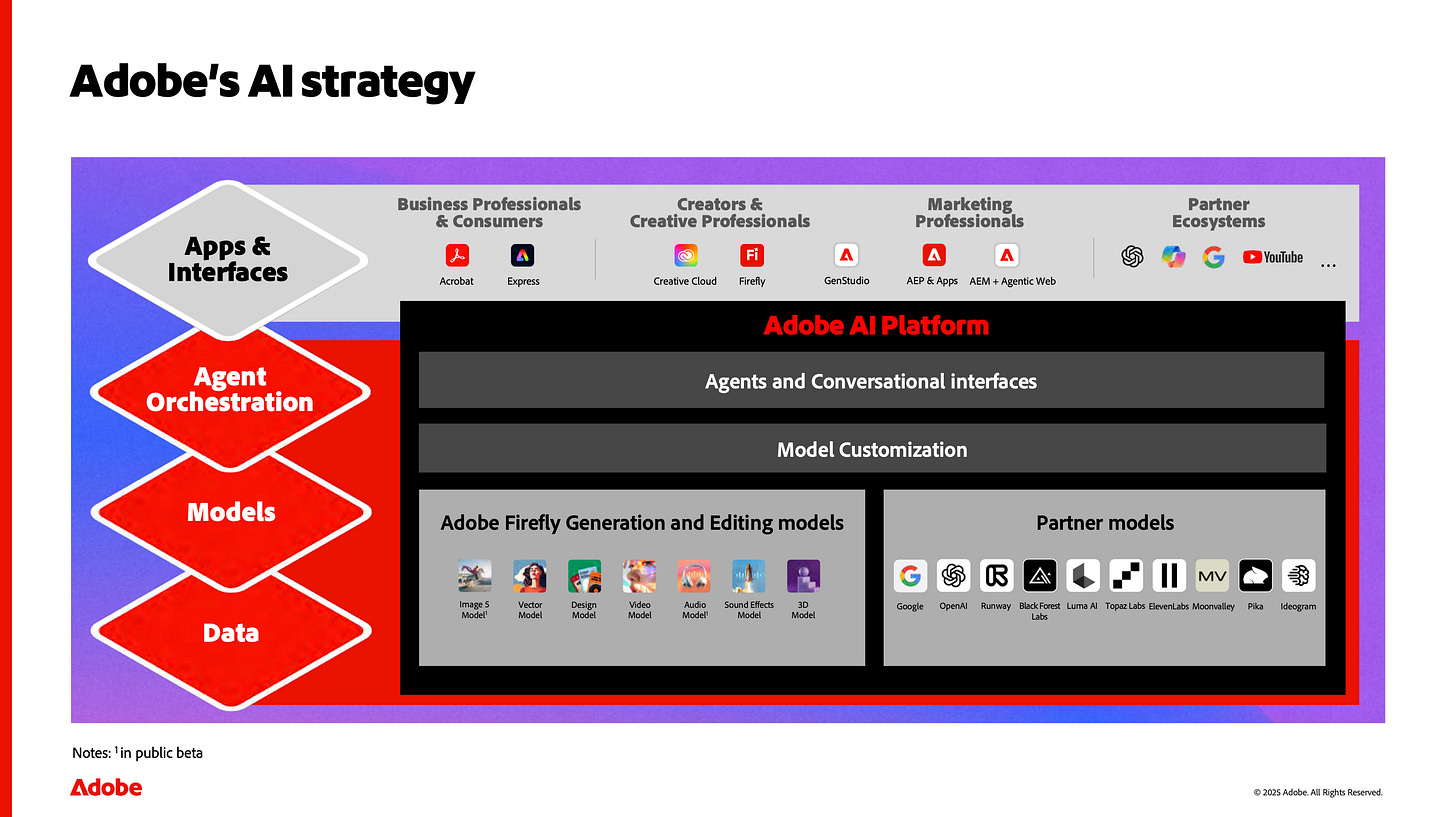

Adobe’s 2025 Investor Presentation - AI Strategy Pathway to Profitability: (2/2)

Adobe turned profitable in the 1990s and has since been consistently expanding its margins.

7. Red Flags and Risks

Lack of an Economic Moat: (0/-2)

Adobe currently has a moat due to its high switching costs, intangible assets, and large recurring customer base.

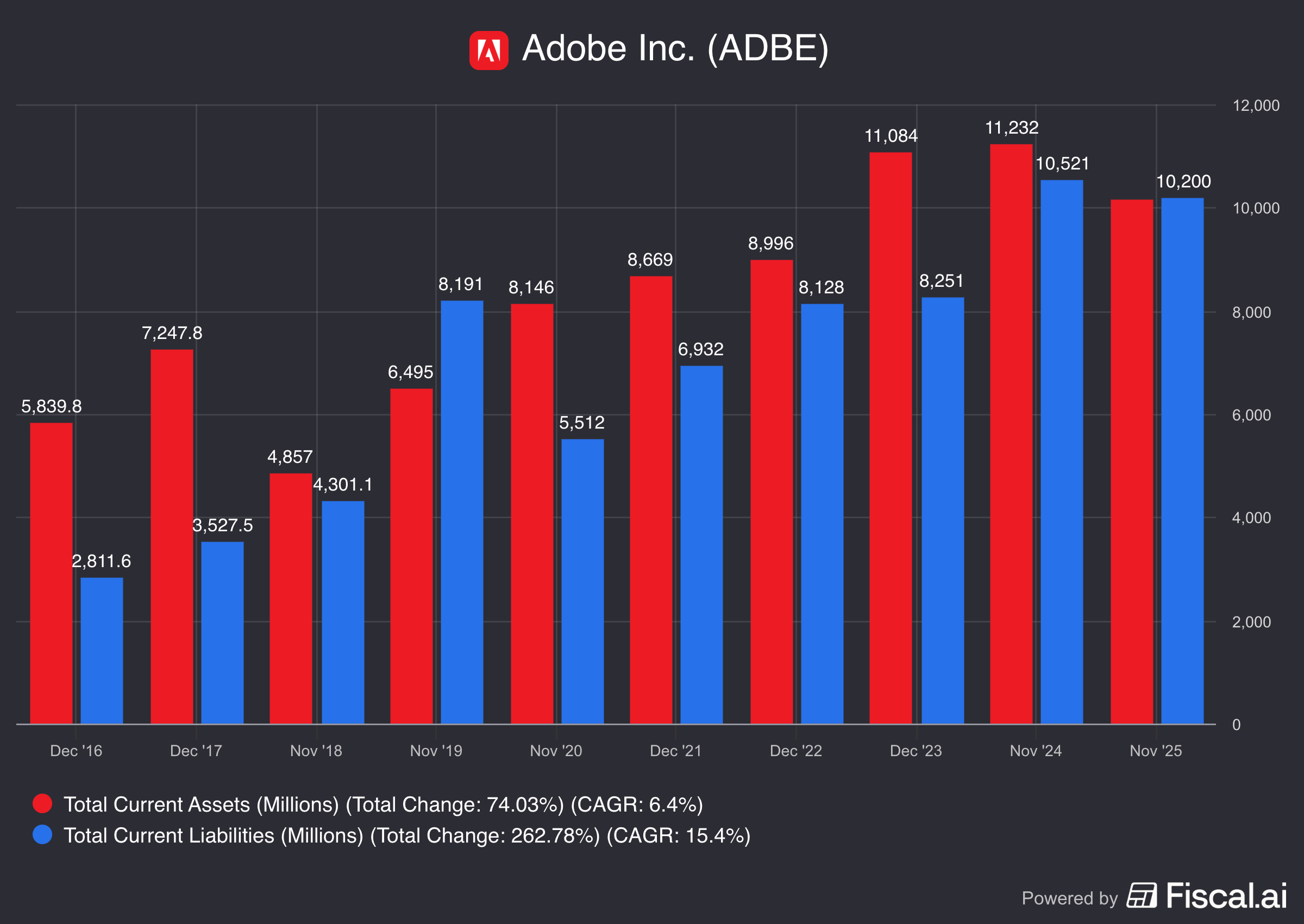

Balance Sheet Risk: (0/-2)

Adobe's balance sheet is solid. As of January 2026 its current assets were $10.2 billion, while its current liabilities amounted to $10.2 billion.

Lack of Profit Visibility: (0/-2)

Adobe turned profitable in the 1990s and has since been consistently expanding its margins.

Regulatory & Geopolitical Risk: (0/-1)

Despite being present in most countries in the world, Adobe is generally perceived as a very responsible company which has not had any major regulatory issues in the past.

Although the US government has closely looked at its subscription cancellation policies and other aspects for possible antitrust practices, these have not yielded any results.

Core Business Disruption: (-1/-1)

The main threat of disruption clearly comes from AI. This is threatening an erosion of Adobe’s long-standing moat which was dependent on the thousands of hours required to master its tools. The new AI tools threaten to remove this barrier, allowing non-specialists to produce high-quality outputs with simple prompts. If the “skill gap” disappears, Adobe’s premium pricing becomes harder to justify.

On the other hand, even if Adobe is able to maintain its premium pricing, as AI significantly boosts productivity, it may allow a single designer with AI to become as productive as five designers. This would allow companies to lower the number of licenses they hire from Adobe, potentially reducing its subscriber count.

Customer Concentration Risk: (0/-1)

Adobe does not have high customer concentration risk as its products are sold directly to thousands of customers.

“For all periods presented, there were no customers that represented at least 10% of net revenue or that were responsible for over 10% of our trade receivables.” - Adobe’s 2024 Annual Report

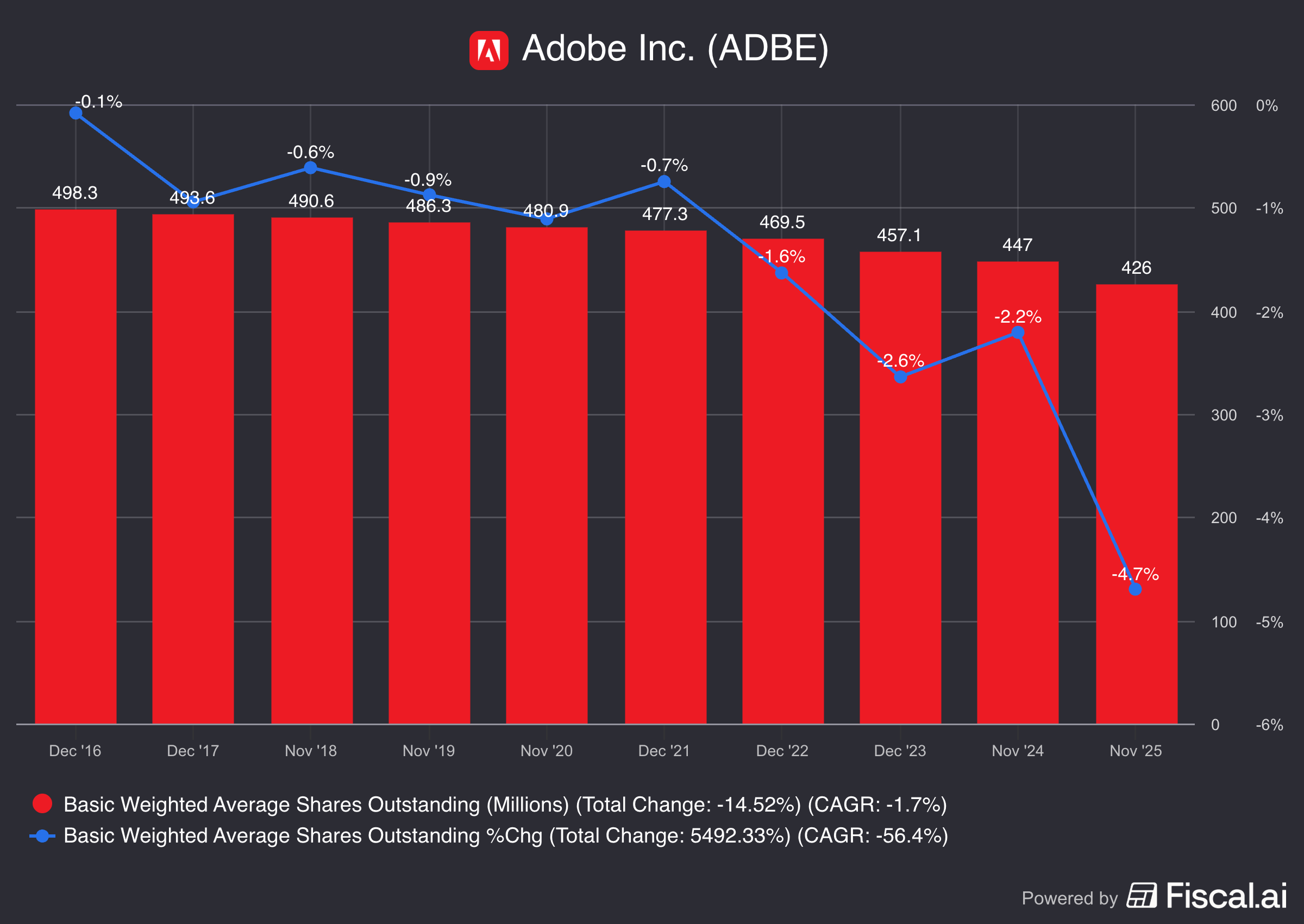

Share Dilution: (0/-1)

Adobe’s total shares outstanding have been consistently decreasing every year since 2016, which a very sharp increase in its share repurchase program in the recent years, due to its perceived undervaluation.

From 2024 to 2025, Adobe reduced its weighted average shares outstanding by 5%, massively returning its generated FCF to investors.

Adobe Quality Score (FINAL):

Adding up the scores and deducting one for potential risk, Adobe scores a total of 17.5/22 points, making it a “High Conviction” business and one which could potentially deserve a deep dive analysis.

We have reviewed Adobe’s incredible fundamentals, which have resulted in the company scoring high on The Compounder Score. However, does this mean that the stock is trading at a valuation where it should be deemed a clear buy or is the risk too high?

The final, essential sections cover:

Comparable Analysis of Adobe’s historic valuation ratios versus its peers.

The Compounder DCF with potential return and intrinsic value estimates based on scenarios.

This part of the analysis is reserved exclusively for our premium subscribers to reward for their amazing support.

Subscribe now to get full access to all our upcoming analyses!

Adobe Valuation: